Written Commentary

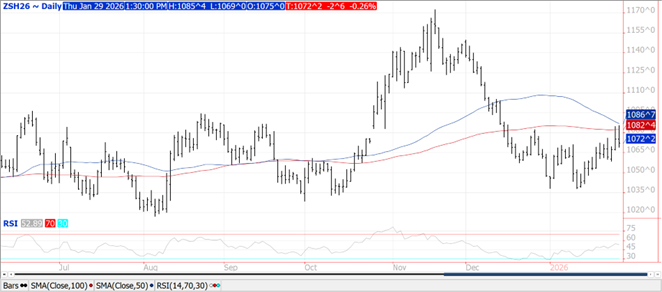

CORN

Prices were $.01-$.02 higher in choppy trade. Spreads weakened. Mch-26 pulled back after trading to its highest level since the January USDA reports. Major MA resistance just below $4.40. Open interest surged 21k contracts yesterday in trade that featured moderately heavy speculative buying. Export sales at 65 mil. bu. were in line with expectations. YTD commitments at 2.271 bil. bu. are up 33% from YA, vs. the USDA forecast of up 12%. Noted buyers were Japan, Mexico and Colombia all buying 13-14 mil. bu. Monthly census exports from Nov-25 were 288 mil. bu. 9 mil. above implied inspection data. Cumulative sales in Q1 the 25/26 MY at 821 mil. bu. are up 60% YOY Pace analysis would suggest the already record USDA forecast at 3.2 bil. bu. is looking low, however aggressive offers from Argentina may cut into US market share the 2nd half of the MY.

SOYBEANS

Prices closed lower across the complex with beans $.01-$.03 lower, meal off $1-$2 while oil was down 25-30 points. Spreads eased across the complex. For a 2nd consecutive session Mch-26 beans rejected trade above its 100 day MA at $10.82 ½. Mch-26 oil pulled back from session highs to close just above $.54 lb. Mch-26 meal is near the midpoint of this week’s range. Spot board crush margins slipped $.04 to $1.73 ½ bu. while bean oil PV held steady at 47.7%. Dry with much above normal temperatures across EC and southern Argentina thru early next week before temperatures cool with better prospects for rain. Soil moisture is in rapid decline. Export sales at 30 mil. were a third of the previous week’s total, however in line with expectations. YTD commitments at 1.244 bil. are down 20% from YA vs. the USDA forecast of down 16%. Sales to China at 233k mt (8.5 mil. bu.) bring total sales to 9.65 mmt with another 3.36 mmt to unknown. Shipments to China are just over 3.5 mmt. Egypt was the only other noted buyer with 6 mil. bu. Meal sales at 464k tons brought YTD commitments to 10,270k tons up 11% YOY vs. the USDA forecast of up 5%. Bean oil commitments are down 50% YOY however in line with the USDA forecast. Monthly census exports from Nov-25 at 158 mil. bu. bring cumulative sales in Q1 of the 25/26 MY to 460 mil. bu. down 44% YOY vs. the USDA forecast of down 16%. To reach the current USDA forecast shipments Dec-25 thru Aug-26 will need to reach 1.115 bil. bu. up 4.5% over YA. Continued shipments to China will help, however likely not enough to reach the current USDA est. of 1.575 bil. bu. Monthly biodiesel and RD production, capacity and feedstock usage data on Friday. Census crush from December after the close on Monday. Soybean O.I. jumped 12k contracts in yesterday’s trade with both products slightly lower.

WHEAT

Prices were $.05-$.08 higher across the 3 classes. CGO Mch-26 jumped out to a 2 month high while also reaching our objective of $1.10 over Mch-26 corn futures. KC Mch-26 also traded to a fresh 2 month high with next resistance at $5.53 ½. Huge range in Mch-26 MIAX as prices closed at session highs up $.07 ½. O.I. in CGO rose just over 4.5k contracts yesterday after speculative traders bought 7k contracts indicating fresh money coming in the long side of the market, not just a speculative short covering rebound. O.I. in KC little changed at down 500 contracts. Export sales at 21 mil. bu. were in line with expectations bringing YTD commitments to 788 mil. bu. up 18% from YA, vs. the USDA forecast of up 9%. By class commitments vs. the USDA forecast are HRW +84% vs. USDA +47%, SRW +8% vs. -2%, HRS down 9% vs. -8%, and white down 1% vs. -5%. Monthly census exports from Nov-25 at 60 mil. bu. were 5 mil. above implied inspection data. Cumulative sales in 6 months of the 25/26 MY at 501 mil. bu. are up 21% YOY vs. the USDA forecast of up 9%. To reach the USDA forecast sales over the 2nd half of the MY need to reach 399 mil. bu. vs. 403 mil. YA.

Charts provided by CQG

Risk Warning: Investments in Equities, Contracts for Difference (CFDs) in any instrument, Futures, Options, Derivatives and Foreign Exchange can fluctuate in value. Investors should therefore be aware that they may not realise the initial amount invested and may incur additional liabilities. These investments may be subject to above average financial risk of loss. Investors should consider their financial circumstances, investment experience and if it is appropriate to invest. If necessary, seek independent financial advice.

ADM Investor Services International Limited, registered in England No. 2547805, is authorised and regulated by the Financial Conduct Authority [FRN 148474] and is a member of the London Stock Exchange. Registered office: 3rd Floor, The Minster Building, 21 Mincing Lane, London EC3R 7AG.

A subsidiary of Archer Daniels Midland Company.

© 2021 ADM Investor Services International Limited.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.