Written Commentary

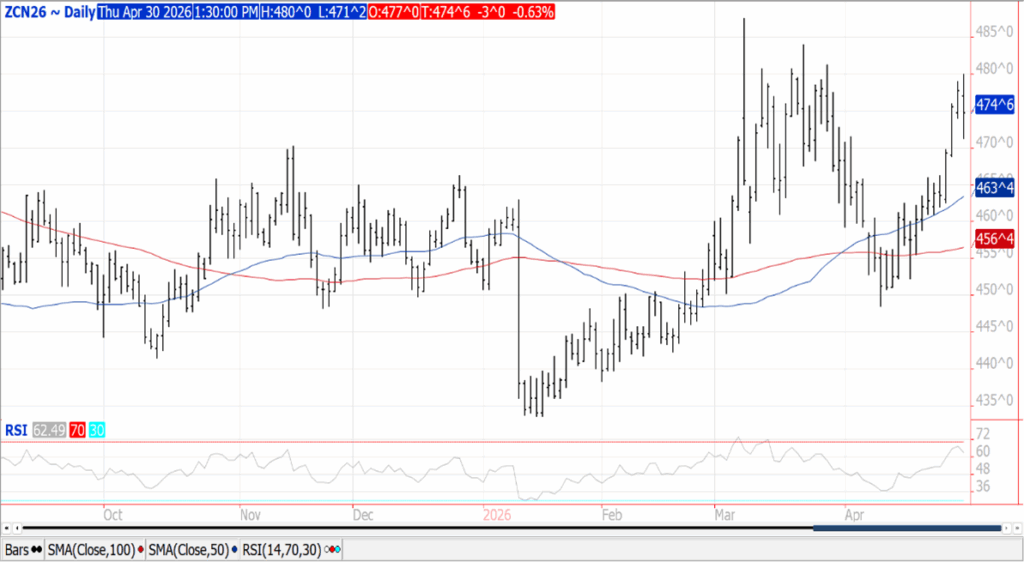

CORN

Prices were down $.02-$.04 in choppy, 2-sided trade. Spreads finished a bit firmer. Both July-26 and Dec-26 traded at new highs for the month. July-26 could not penetrate the upper end of its $4.50-$4.80 range while Dec-26 held just below $5.00 while ending its run of consecutive higher closes at 9. Deliveries against May-26 corn were 19 contracts. Ethanol production has been below expectations the past 2 weeks. Heavy rains from earlier this week will likely not slow corn plantings for long. Export sales at 63 mil. bu. were in line with expectations and brought old crop commitments to 2.980 bil. bu. up 29% from YA, vs. the USDA forecast of up 15.5%. Commitments represent 90% of the USDA forecast, vs. the historical average of 86%. Noted buyers were Colombia – 17 mil. while Mexico, Venezuela and unknown all bought 9-10 mil. US corn acres in drought slipped another 2% to 25%, the lowest since Sept-25. The US House passed a new Farm Bill which now moves on to the Senate. The provision to allow voluntary E-15 blending year-round was excluded. The EU Commission held their 26/27 corn production forecast unchanged at 61.2 mmt, up from 56.8 mmt YA, while also keeping their import forecast at 19.3 mmt vs. 19.5 YA.

SOYBEANS

Prices were mixed with beans ranging from $.01 ½ lower to $.02 higher, meal was down $3-$5 while oil was 40-100 points higher. Bean and oil spreads were mixed while meal spreads weakened. New high for the May/July oil spread. For now July-26 beans rejected trade above $12. Nov-26 beans reached a 2-year high. New contracts highs in bean oil with the spot contracts soaring to a fresh 3 ½ year. July-26 meal violated support at its 50-day MA at $319.60. Surging D4 RIN values along with higher prices for alternative feedstocks has kept bean oil the feedstock of choice in green diesel production. Energy prices experienced 2-sided trade after reaching fresh contract highs for the June-26 contracts in WTI crude oil, RBOB and heating oil in overnight trade. Spot board crush margins slipped $.01 to $3.67 bu. while bean oil PV surged to a new all-time high at 54.2%. There were no deliveries against May-26 beans or meal while only 400 against May-26 oil. Export sales at 10 mil. were at the low end of expectations. YTD commitments at 1.425 bil. are down 18% from YA in line with the USDA forecast. Sales to China have reached 11.735 mmt with another 1.4 to unknown. Shipments to China are up to 10.4 mmt. YTD meal sales at 14.35 mmt are up 16% YOY vs. the USDA up 6%. Bean oil sales at 810 mil. lbs. down 62% YOY vs. USDA forecast of down 52%. EIA data showed bean oil usage for the production of biofuels jumped 8% to 1.058 bil. Lbs. in Feb-26. Oct-25 thru Feb-26 usage at 4.831 bil. Lbs. is unchanged from 24/25 vs. the USDA forecast of up 19%. Bean oil represented 44.3% of feedstock usage, up from 42.6% Jan-26 and the highest since July-23. Usage Mch-26 thru Sept-26 will need to average 1.310 bil. Lbs. per month to reach USDA est. D4 RIN generation in Mch-26 were up 35% over Feb-26, suggesting a sizeable bump up in biodiesel and RD production, and likely bean oil usage.

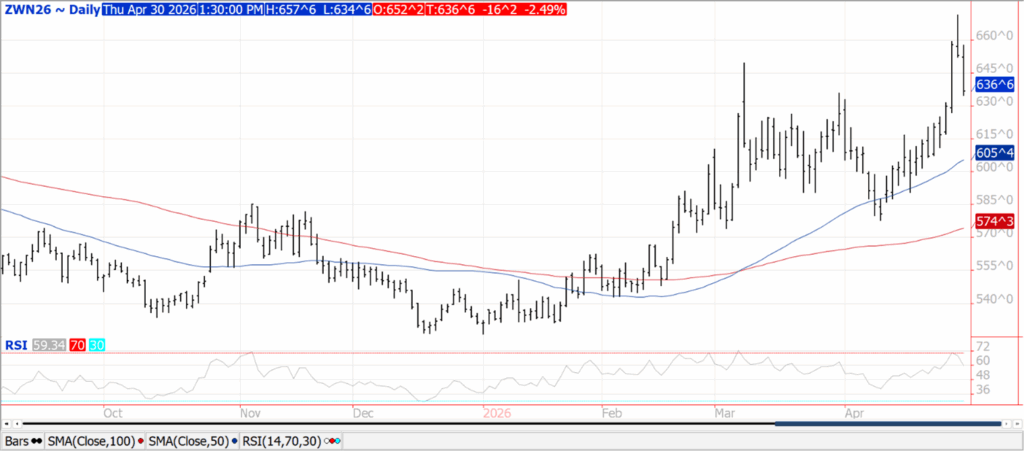

WHEAT

Prices were down $.10-$.16 as the wheat market experienced spillover selling from yesterday’s weak close. Spreads weakened in all 3 classes with most spreads in CGO hitting new lows. CGO July-26 was down $.16 ¼ at $6.36 3/4, KC July-26 was $.11 ¼ lower at $6.93 ½, while MIAX July-26 was off $.10 at $7.05 ¾. Deliveries against CGO wheat were 400 contracts while 578 for KC wheat. Export sales at 14 mil. bu were in line with expectations. Old crop commitments at 907 mil. bu. are up 16% from YA, vs. the USDA forecast of up 9%. Winter wheat acres in drought fell 1% to 69% while Spring wheat acres in drought held steady at 18%. SovEcon raised their Russian wheat export forecast for 25/26 MY .9 mmt to 47.4 mmt, well above the USDA forecast of 44.5 mmt. SovEcon also raised their 26/27 export est. 1.4 mmt to 45.2 mmt. The EU Commission raised their 26/27 production forecast 1.4 mmt to 127.3 mmt while lowering their export forecast .35 mmt to 30.

Risk Warning: Investments in Equities, Contracts for Difference (CFDs) in any instrument, Futures, Options, Derivatives and Foreign Exchange can fluctuate in value. Investors should therefore be aware that they may not realise the initial amount invested and may incur additional liabilities. These investments may be subject to above average financial risk of loss. Investors should consider their financial circumstances, investment experience and if it is appropriate to invest. If necessary, seek independent financial advice.

ADM Investor Services International Limited, registered in England No. 2547805, is authorised and regulated by the Financial Conduct Authority [FRN 148474] and is a member of the London Stock Exchange. Registered office: 3rd Floor, The Minster Building, 21 Mincing Lane, London EC3R 7AG.

A subsidiary of Archer Daniels Midland Company.

© 2021 ADM Investor Services International Limited.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.