Written Commentary

London Wheat Report

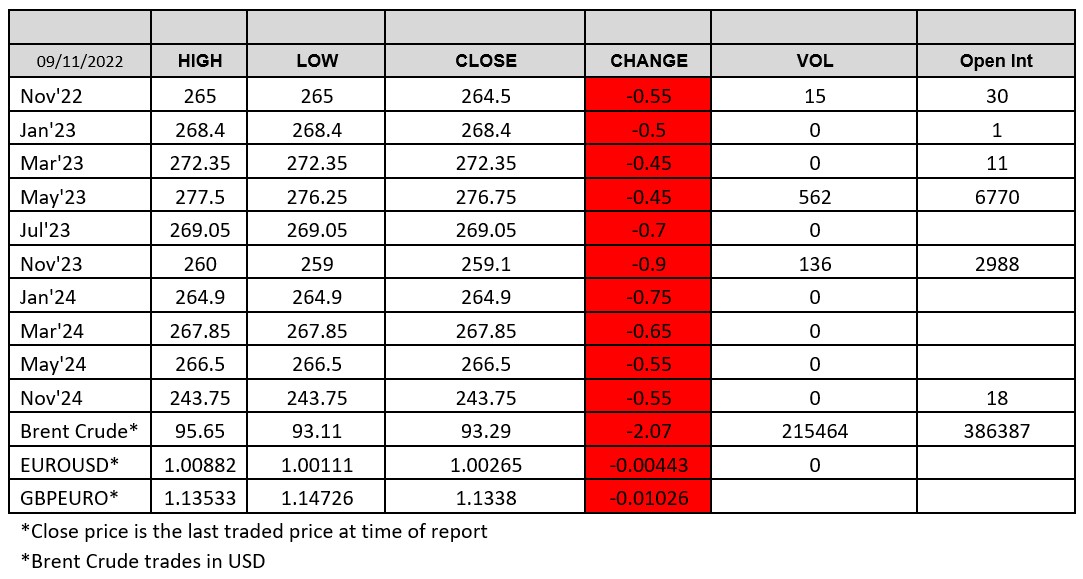

Source: FutureSource

WASDE day today. Nothing overly too exciting or intriguing.

The outlook for 2022/23 U.S. wheat this month is for stable supplies, increased domestic use, unchanged exports, and slightly lower ending stocks. US domestic usage wheat has been upped while exports remain unchanged. Ending stocks are pegged at around 571M bushels which is the lowest level since 2007/08.

The global wheat outlook for 2022/23 is for increased supplies, consumption, trade, and ending stocks. Supplies are projected up 1.3 million tons to 1,059.0 million based on increases in beginning stocks and production. World production is raised 1.0 million tons to 782.7 million as larger production in Australia, Kazakhstan, and the UK more than offsets declines in Argentina and the EU. and boosted yields, following widespread favourable conditions earlier in the growing season. Argentina production is lowered as continued widespread dry conditions through most of October further eroded yield potential, especially in northern areas. Increase in global trade with higher exports from Aussie, Kazakhstan and the UK more than offset a reduction in export by Argentina. Projected global ending stocks are increased 0.3 million tons to 267.8 million, with increases for Australia and India and a decrease for the EU accounting for most of the change.

This month’s 2022/23 U.S. corn outlook is for higher production, larger feed and residual use, and greater ending stocks. Global coarse grain production for 2022/23 is forecast fractionally lower at 1,459.5 million tons. corn production is forecast lower as declines for the EU, South Africa, Philippines, and Nigeria are partly offset by increases for Angola, Mali, Pakistan, Turkey, and Senegal. EU production is down, but by nowhere near the extent to where it should be after the French harvest downgrades.

The U.S. soybean outlook for 2022/23 is for increased production, crush, and ending stocks. The U.S. season-average soybean price for 2022/23 is forecast at $14.00 per bushel, unchanged from last month. Global oilseed production for 2022/23 is projected at 645.6 million tons, down 1.0 million from last month. Lower soybean, sunflower seed, and cottonseed production is partly offset by higher rapeseed. Area harvested for Argentina is reduced reflecting in country estimates. Sunflower seed production is reduced for Ukraine on lower reported yields. Global rapeseed production is raised 1.0 million tons to 84.8 million on higher yields for Australia and the EU.

Contact the ADMISI Grains and Oilseeds Derivatives Brokerage team

Hanne Bell, Ryan Easterbrook, Dominic Enston and Aaron Stockley-Isted

Phone: +44 (0)20 7716 8477 or +44 (0)20 7716 8140 Email: intl.grains@admisi.com

Risk Warning: Investments in Equities, Contracts for Difference (CFDs) in any instrument, Futures, Options, Derivatives and Foreign Exchange can fluctuate in value. Investors should therefore be aware that they may not realise the initial amount invested and may incur additional liabilities. These investments may be subject to above average financial risk of loss. Investors should consider their financial circumstances, investment experience and if it is appropriate to invest. If necessary, seek independent financial advice. ADM Investor Services International Limited, registered in England No. 2547805, is authorised and regulated by the Financial Conduct Authority [FRN 148474] and is a member of the London Stock Exchange. Registered office: 3rd Floor, The Minster Building, 21 Mincing Lane, London EC3R 7AG. A subsidiary of Archer Daniels Midland Company.

© 2022 ADM Investor Services International Limited

Risk Warning: Investments in Equities, Contracts for Difference (CFDs) in any instrument, Futures, Options, Derivatives and Foreign Exchange can fluctuate in value. Investors should therefore be aware that they may not realise the initial amount invested and may incur additional liabilities. These investments may be subject to above average financial risk of loss. Investors should consider their financial circumstances, investment experience and if it is appropriate to invest. If necessary, seek independent financial advice.

ADM Investor Services International Limited, registered in England No. 2547805, is authorised and regulated by the Financial Conduct Authority [FRN 148474] and is a member of the London Stock Exchange. Registered office: 3rd Floor, The Minster Building, 21 Mincing Lane, London EC3R 7AG.

A subsidiary of Archer Daniels Midland Company.

© 2021 ADM Investor Services International Limited.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.