Written Commentary

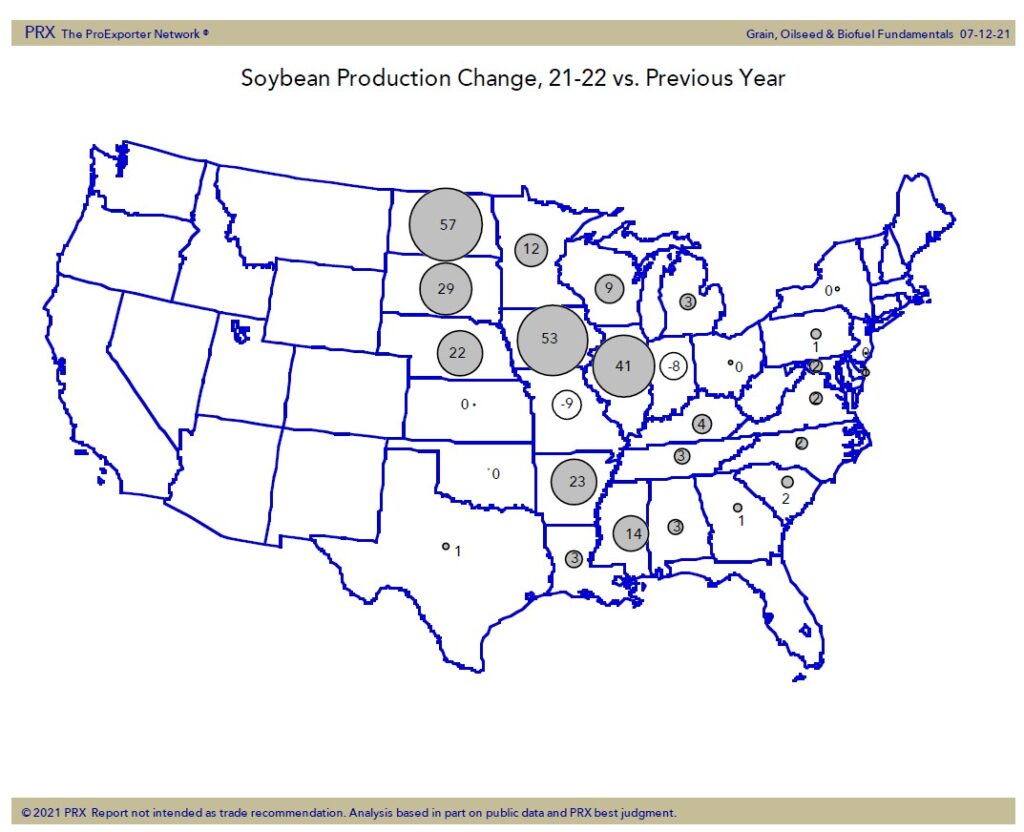

SOYBEANS

Soybean futures ended higher. USDA August soybean numbers were not considered bullish but more daily US soybean sales to China offered support. As expected USDA dropped US 20/21 demand 25 mil bu and raised carryout to 160. USDA decided that US 21/22 carryout will be 155. USDA then plugged in the lower crop of 4,339 and dropped crush 20 and exports 20. July World soybean plus soymeal exports were only 13.0 mmt SBME vs 14.8 ly. Oct-July exports are 143.5 mmt vs 146.2 ly. USDA new Oct-Sep goal is 176.9 vs 175.1 ly. Brazil Oct-July soybean exports were 69.5 mmt vs 82.2 ly. US was 53.2 vs 37.0 ly. Argentina soybean exports are forecasted at only 3.7 mmt vs 10.0 ly. US/Brazil/Arg Oct-July soymeal exports were near 47.1 mmt cs 47.5 ly. US NOPA soybean crush is est near 159.0 vs 172.8 ly.

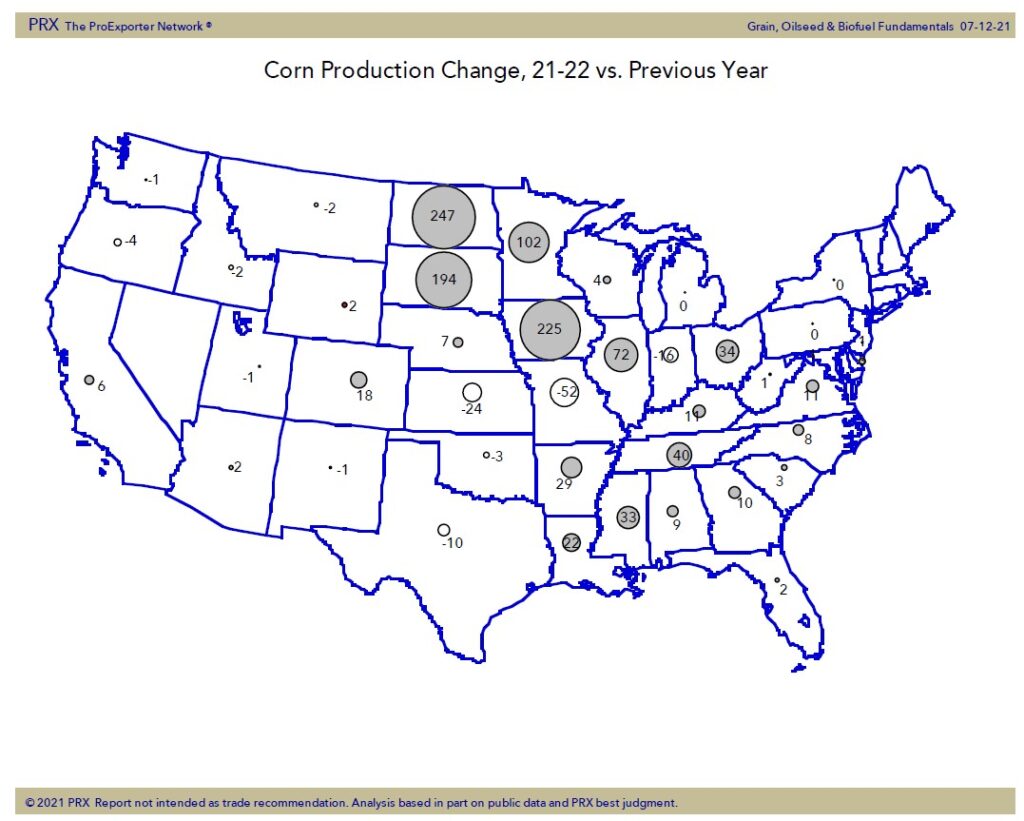

CORN

Corn ended near unchanged. CZ ended near 5.73. Range was 5.66 to 5.82. CU settled near the 50 day moving average. CU had an inside day. USDA crop report high was 5.89. Some feel CZ may struggle to trade higher through harvest. Key support remains near 5.40. Over the next 2 weeks GFS weather maps hint of rains falling across US plains and NW. Some feel this could add bushels to the corn crop versus USDA August guess. Others feel fact USDA may be low in their estimate of US 21/22 corn exports suggest final US 21/22 carryout could be below USDA est. It feels like in corn, USDA decided that US 21/22 corn carryout will be 1,242 mil bu first. They plugged in the new crop est of 14,750 and the decided to drop exports 100 mil bu from July and 375 mil bu below this year. They also decided to drop feed use 100 mil bu from July and 100 mil bu below this year. They est 21/22 ethanol use at 5,200 vs 5,075 this year. Most are using exports closer to 2,800 which would drop carryout closer to 850 and suggest nearby corn futures could trade over 6.00 after harvest. US farmer was an active seller on the USDA report rally. In some locations, they may be sold out of old crop and up to 60 pct sold of new crop. FSA farm enrollment acres suggest USDA may be low in their est of US 2021 corn and sorghum acres. Next week, Pro Farmer will have their annual crop tour across US Midwest.

WHEAT

USDA August report is now behind us. USDA answered some questions about US farmer white winter wheat, Russia wheat and Canada wheat crop prospects. Russia wheat crop estimate was the biggest surprise. Some feel that the lower World wheat crops supply outlook could continue to support prices. Bulls could even see nearby Chicago wheat testing 8.50-9.00 Dec-Feb. Tight US supply suggest US 2022 wheat acres need to increase or US 2022/23 wheat carryout could drop below 500 mil bu. USDA now est World 20/21 wheat crop at 777 mmt vs 792 in July, domestic demand 786 mmt vs 784 ly and exports 198 vs 201 last year. End stocks are 279 vs 291 previous and 288 ly. World exporters stocks 49 mmt vs 57 in July. WZ made new highs near 7.86. KWZ near 7.69. MWZ near 9.37. USDA est US 21/22 HRW end stocks near 346 mil bu vs 426 ly, SRW 104 vs 85. HRS 116 vs 235 and white winter 40 vs 70. White winter exports could drop to 160 from 270 ly.

Monthly nearby Chicago wheat futures chart

Risk Warning: Investments in Equities, Contracts for Difference (CFDs) in any instrument, Futures, Options, Derivatives and Foreign Exchange can fluctuate in value. Investors should therefore be aware that they may not realise the initial amount invested and may incur additional liabilities. These investments may be subject to above average financial risk of loss. Investors should consider their financial circumstances, investment experience and if it is appropriate to invest. If necessary, seek independent financial advice.

ADM Investor Services International Limited, registered in England No. 2547805, is authorised and regulated by the Financial Conduct Authority [FRN 148474] and is a member of the London Stock Exchange. Registered office: 3rd Floor, The Minster Building, 21 Mincing Lane, London EC3R 7AG.

A subsidiary of Archer Daniels Midland Company.

© 2021 ADM Investor Services International Limited.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.