Written Commentary

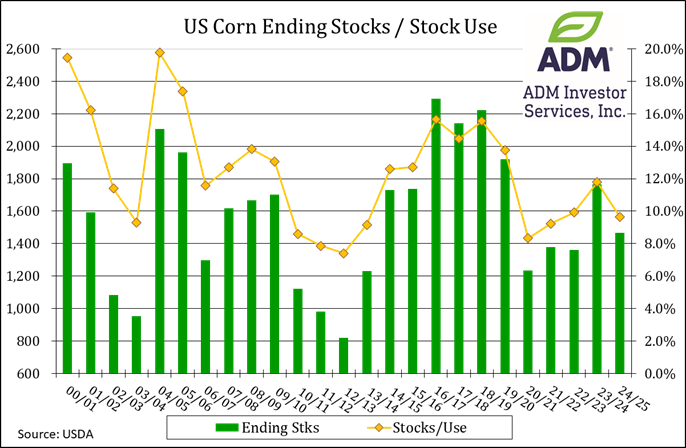

CORN

Prices ranged from $.04-$.09 higher closing near session highs led by old crop futures. July-25 stretched out to 6 week high, taking out both its 50 day MA and high from March. New crop Dec-25 held in check with US farmers expected to plant nearly 5 mil. more acres than YA. I look for old crop to continue to outperform new crop. The USDA cut ending stocks 75 mil. bu. 1.465 bil. 45 mil. below the Ave. trade guess. Feed usage was lowered 25 mil. exports raised 100 mil. to 2.550 bil. The Ave. Farm Price was left unchanged at $4.35 bu. No changes to SA production or Chinese imports. Mexico’s imports rose .5 mmt to a record 25 mmt. Global stocks were cut 1.3 mmt to 287.65 mmt, due to lower US stocks. Old crop prices have recovered just over half of the liquidation break from late Feb. to early March.

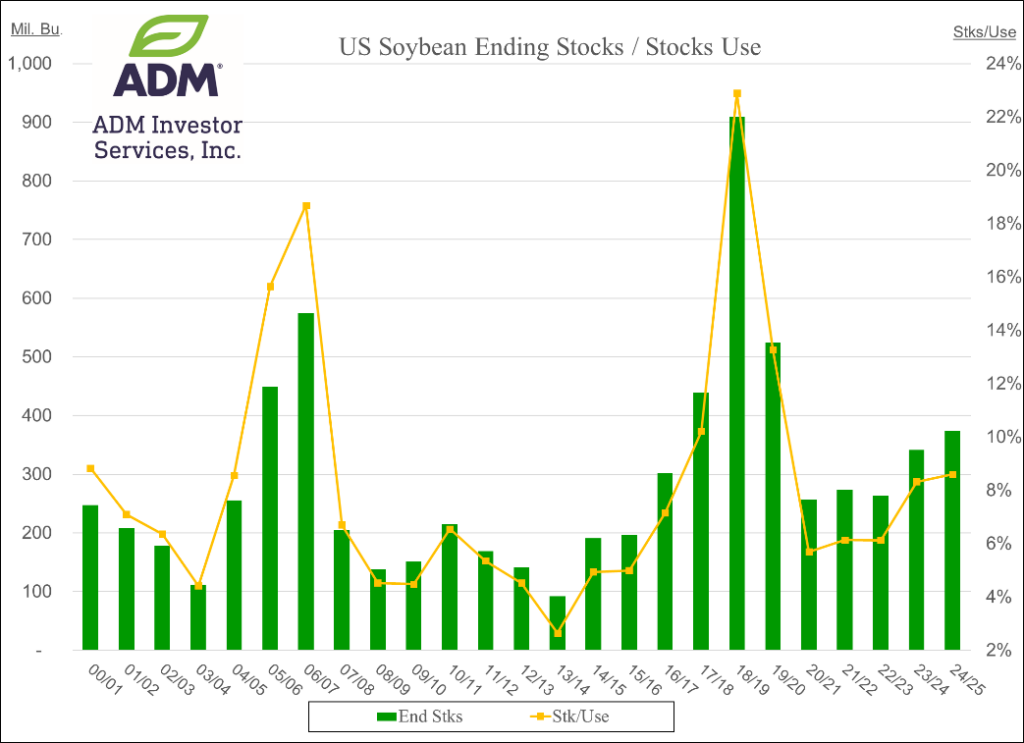

SOYBEANS

Prices were higher across the complex with beans ranging from $.07-$.16 higher led by old crop, meal was up $3-$4, while oil rebounded to close 10-15 higher. July-25 futures worked back into a gap from last week, however stalled and closed very near its 100 day MA at $10.39 ½. July-25 meal posted its highest close in 3 weeks as speculators continue to lighten up on their record short position. Impressive that July-25 oil was able to scratch out a higher close despite all day weakness in energy prices. By mid-morning the White House announced tariffs on Chinese imports were now 145%, up from 125% yesterday. Rains are needed across SC growing regions of Brazil before the dry season kicks in next month. Improved chances for rains in week 2 of the outlook did little to slow the strength in corn. US soybean stocks were cut 5 mil. bu. to 375 mil., in line with expectations. Imports were raised 5 mil. with those added supplies more than offset by a 10 mil. bu. increase in crush. The Ave. US Farm Price was left unchanged at $9.95 bu. Bean oil stocks were cut 80 mil. lbs. to 1.451 bil. lbs. Exports were raised 500 mil. lbs. offset by domestic usage down 300 mil. while production was up 120 mil. given the added crush. Of the lower domestic usage, 200 mil. lbs was from lower usage for biofuel production. While there were no changes to SA production for the 24/25 crops, last year’s production in Brazil was increased 1.5 mmt to 154.5 mmt. These added supplies from last year were largely absorbed by higher crush in the 24/25 MY. Argentina was up .5 mmt to 50.1 mmt, while Brazil’s crush rose 1 mmt to 61.1 mmt. Global stocks for 24/25 did rise 1.1 mmt to 122.5 mmt, slightly above expectations.

WHEAT

The weakling within the Ag. space as prices ranged from $.02-$.10 lower with KC futures the downside leader. In the near term little to no rain for the US plains and WCB will help corn planting get underway. Week 2 of the outlook brings better prospects for rain in the Southern plains. Outside day down in July-25 KC futures, unable to hold early strength above its 100 day MA. US ending stocks increased 25 mil. bu. to 846 mil. 20 mil. above expectations. Imports rose 10 mil. bu. while exports were lowered 15 mil. HRW stocks jumped up 26 mil., spring wheat stocks rose 16 mil., while durum was down 13 mil. SRW wheat stocks (CGO) held steady at 116 mil. bu. The Ave. US Farm Price was unchanged at $5.50 bu. Global stocks were up .6 mmt to 260.7 mmt. Russian exports were down 1 mmt, Ukraine/Canada up .5 mmt, EU/Australia down .5 mmt. US WW area in drought dropped 5% LW to 32%, still well above the 15% from YA. Spring wheat area in drought rose 4% to 43%, nearly double the 22% from YA. May-25 CGO wheat spread over May-25 corn plunged $.13 today to a new low at $.55 bu. as abundant wheat stocks will try to work more into feed rations.

Charts provided by QST.

>>See more market commentary here.

Risk Warning: Investments in Equities, Contracts for Difference (CFDs) in any instrument, Futures, Options, Derivatives and Foreign Exchange can fluctuate in value. Investors should therefore be aware that they may not realise the initial amount invested and may incur additional liabilities. These investments may be subject to above average financial risk of loss. Investors should consider their financial circumstances, investment experience and if it is appropriate to invest. If necessary, seek independent financial advice.

ADM Investor Services International Limited, registered in England No. 2547805, is authorised and regulated by the Financial Conduct Authority [FRN 148474] and is a member of the London Stock Exchange. Registered office: 3rd Floor, The Minster Building, 21 Mincing Lane, London EC3R 7AG.

A subsidiary of Archer Daniels Midland Company.

© 2021 ADM Investor Services International Limited.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.