Written Commentary

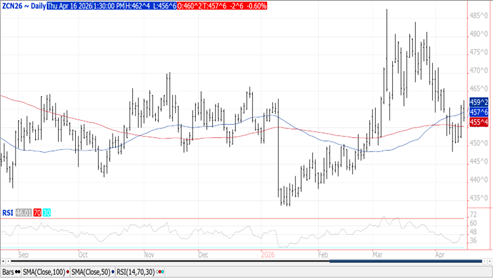

CORN

Prices pulled back late settling $.01-$.03 lower. Spreads also weakened. July-26 closed back below its 50-day MA with next support at the 100-day MA at $4.55 ½. Dec-26 was down $.01 ¼ at $4.76 ¾. Plantings in the SE half of the Midwest are moving along at a rapid pace while little activity in the soaked northern Midwest. Yesterday’s ethanol production at 329 mil. gallons was above expectations as processing margins remain robust. While speculative traders were healthy buyers of nearly 18k contracts yesterday, O.I. in corn fell by just over 10k. Export sales at 57 mil. bu. were in line with expectations and brought old crop commitments to 2.866 bil. bu. up 29% from YA, vs. the USDA forecast of up 15.5%. Commitments represent 87% of the USDA forecast, above the historical average of 83%. Noted buyers were Japan–16 mil., Korea–13 mil. and Mexico–7 mil. The BAGE raised their Argentine production forecast 4 mmt to 61 mmt, well above the USDA est. of 52 mmt, however still below the Rosario Grain Exchange est. of 67 mmt.

SOYBEANS

Prices were sharply mixed with beans ranging from $.03 lower to $.02 higher, meal was down $2-$4 while bean oil jumped 135-175 points. Bean spreads weakened while product spreads firmed. July-26 beans may be stuck between $11.50-$12.00 until the Trump/Xi meeting next month. Inside trade for July-26 meal. July-26 oil filled the gap from earlier this month with next resistance at its contract high of 70.12. Spot board crush margins surged another $.18 to $3.30 ½ bu., nearly the modern day high of $3.40 from Oct-22. With yesterday’s NOPA crush slightly below expectations, oil stocks fell to 2.04 bil. lbs. The implied census crush at 231 mil. bu. resulted in the daily crush rate slipping to 7.45 mil. bu. a day, down from the all-time high in Feb-26 of 7.64 mbd. Export sales at 9 mil. were at the low end of expectations. YTD commitments at 1.402 bil. are down 18% from YA in line with the revised USDA forecast. Commitments represent 89% of the USDA forecast vs. historical Ave. of 92%. Commitments to China are at 11.5 mmt with another 1.56 mmt to unknown. Shipments to China are now 9.64 mmt. Meal sales at 254k tons were at the low end of expectations and bring YTD commitments to 13.9 mmt up 17% YOY vs. the USDA up 6%. Bean oil sales at 2.4 mil. lbs. bring YTD commitments to 799 mil. lbs. down 62% YOY vs. USDA forecast of down 52%. The BAGE kept their production forecast steady at 48.5 mmt while reporting harvest at 6%.

WHEAT

Prices ranged from $.05-$.17 higher across the 3 classes with KC futures the leader to the upside. KC July-26 stalled after trading into fresh 13 month high. KC July-26 premium over July-26 CGO jumped out to a new high at $.49 bu. Algeria reportedly bought 400k mt of durum with prices ranging from $322-$334/mt CF, depending on vessel size. Their last purchase in Dec-25 was around $315/mt. The Western plains and Nebraska continue to miss out on needed precipitation. While drought in HRW areas deepen, SRW areas in drought continue to ease. Export sales at 8.5 mil. bu. were below expectations. YTD commitments at 896 mil. bu. are up 14% YOY vs. the USDA forecast of up 9%. By class commitments vs. the USDA forecast is HRW +59% vs. USDA up 49%, SRW +6% vs. +2%, HRS -5% vs. -8% and white -5% vs. -10%.

Charts provided by CQG

Risk Warning: Investments in Equities, Contracts for Difference (CFDs) in any instrument, Futures, Options, Derivatives and Foreign Exchange can fluctuate in value. Investors should therefore be aware that they may not realise the initial amount invested and may incur additional liabilities. These investments may be subject to above average financial risk of loss. Investors should consider their financial circumstances, investment experience and if it is appropriate to invest. If necessary, seek independent financial advice.

ADM Investor Services International Limited, registered in England No. 2547805, is authorised and regulated by the Financial Conduct Authority [FRN 148474] and is a member of the London Stock Exchange. Registered office: 3rd Floor, The Minster Building, 21 Mincing Lane, London EC3R 7AG.

A subsidiary of Archer Daniels Midland Company.

© 2021 ADM Investor Services International Limited.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.