Written Commentary

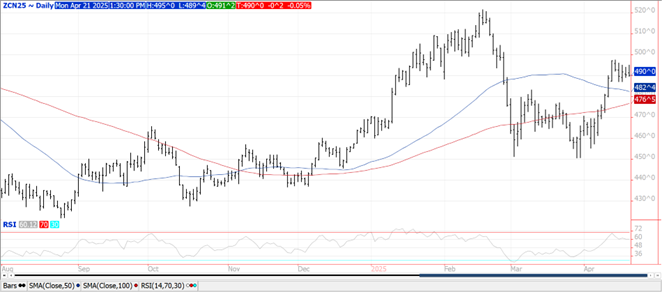

CORN

Prices ranged from steady to $.02 lower in choppy 2 sided trade. Spreads were mixed. First resistance for July-25 is at LW’s high at $4.97 ½ with longer term resistance at $5.21 ½. Support is at LW’s low at $4.87. Early strength the result of a sharp plunge in the US $$$ that gapped lower carving out a fresh 3 year low. The battle between Pres. Trump and Fed. Reserve Chair Powell is likely to intensify as the Fed remains reluctant to cut rates now, choosing to see additional data on how the Trump Administrations use of tariffs will impact consumer prices. Export inspections at 67 mil. bu. were above expectations and well above the 46 mil. bu. needed per week to reach the USDA forecast of 2.550 bil. bu. YTD inspections at 1.544 bil. are up 29% from YA vs. the USDA forecast of up 11%. Largest takers were Mexico – 19 mil., Japan – 17 mil., and S. Korea with 8 mil. Last week MM’s were net buyers of 71k contracts of corn, extending their long position to nearly 125k contracts, still well below the Feb-25 high at 364k contracts. Index funds were also net buyers of nearly 42k contracts, ending a run of 7 consecutive weeks of being net sellers.

SOYBEANS

Prices were lower across the complex with beans down $.06-$.08, meal was off $3 while oil was steady to down 10 points. Spreads across the complex were mixed. July-25 beans held within last week’s range while barely holding above MA support just $10.40. Spot board crush margins held steady at $1.41 per bu. however bean oil PV jumped out to a 3 week high at 44.9%. Agricultural futures also drew support overnight from the USTR announcement on Friday that Trump Administrations tax on Chinese vessels will not begin until the middle of Oct-25 and will only be applied to Chinese owed/made vessels which reportedly acct. for just over 10% of the global fleet. Weekend rains were pretty much as expected with the heaviest amounts centered on the southern and central Midwest. Dry across much of the northern plains, western half of NE and western third of KS. This week will feature good rain’s across much of the nation’s midsection with heaviest totals in the southern plains and the central and WCB. Slightly lower amounts for the Great Lakes region. Normal to above normal temperatures will spread over much of the Midwest. Soybean inspections at 20 mil. bu. were in line with expectations and well above the 5 mil. needed per week to reach the USDA forecast of 1.825 bil. bu. YTD inspections at 1.568 bil. are up 11% from YA vs. USDA forecast of up 8%. China took only 2.5 mil. bu. with 6.4 mil. going to Egypt and 4 mil. to Mexico. Last week MM’s were big buyers across the complex buying nearly 77k contracts of beans, 11k bean oil and just over 28k meal. MM’s flipped their net position on soybeans back to net long just over 26k. Chinese imports of US beans in Mch-25 at 2.44 mmt were well above the 2.18 mmt in Mch-24. The US share of their Mch-25 imports at 69.5% is up from 39.3% in Mch-24 as they loaded up ahead of anticipated higher tariffs.

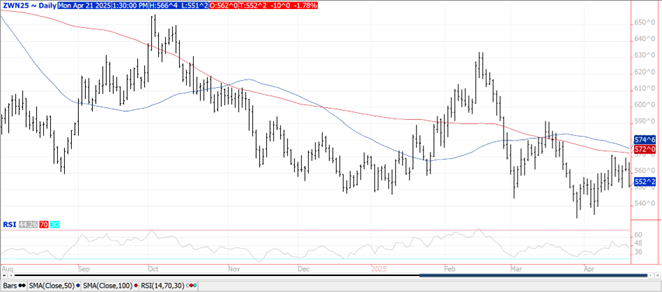

WHEAT

Prices were $.06-$.10 lower across the 3 classes today. Spreads also weakened. July-25 CGO held above LW’s low while KC July-25 matched its low for the month. July-25 MGEX fell to a fresh 2 week low. Export inspections at 19 mil. bu. were above expectations however in line with the amount needed per week to reach the USDA forecast of 820 mil. bu. YTD inspections at 691 mil. are up 14% from YA, vs. the USDA forecast of up 16%. MM’s were net buyers across all 3 classes of wheat LW buying 7.7k in MGEX, 5.7k in CGO and 2.5k in KC. In total MM’s remain a healthy short across the wheat market at 165k contracts combined. IKAR reports the average export price for Russian wheat ended LW between $250-$252/mt, little changed from the previous week. SovEcon reports Russia exported 450k mt of wheat LW, down from 470k the previous week.

Charts provided by QST.

>>See more market commentary here.

Risk Warning: Investments in Equities, Contracts for Difference (CFDs) in any instrument, Futures, Options, Derivatives and Foreign Exchange can fluctuate in value. Investors should therefore be aware that they may not realise the initial amount invested and may incur additional liabilities. These investments may be subject to above average financial risk of loss. Investors should consider their financial circumstances, investment experience and if it is appropriate to invest. If necessary, seek independent financial advice.

ADM Investor Services International Limited, registered in England No. 2547805, is authorised and regulated by the Financial Conduct Authority [FRN 148474] and is a member of the London Stock Exchange. Registered office: 3rd Floor, The Minster Building, 21 Mincing Lane, London EC3R 7AG.

A subsidiary of Archer Daniels Midland Company.

© 2021 ADM Investor Services International Limited.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.