Written Commentary

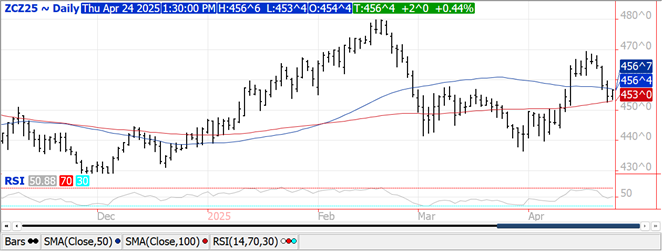

CORN

Prices ranged from $.02-$.05 higher with old crop the leader to the upside. Old crop spreads strengthened while new crop slipped. After bouncing off its 100 day MA support yesterday, July-25 has rebounded back above its 50 day MA today. Inside trade for Dec-25. Exports at 45 mil. bu. were in line with expectations. Old crop commitments at 2.273 bil. are up 26% from YA, vs. the USDA forecast of up 11%. Current commitments represent 89% of the USDA forecast, above the historical average of 86%. Japan was the largest buyer with 25 mil. bu. however 6 mil. were switched from unknown. Mexico bought 5 mil. with 4 mil. each to Colombia and Portugal. The BAGE kept their Argentine production forecast unchanged at 49 mmt, just below the USDA forecast of 50 mmt. Harvest only advanced 2% LW to 30% complete.

SOYBEANS

Prices were mixed across the complex with beans $.08-$.13 higher, meal was down $1-$2 while oil surged 175 points. Something brewing on biofuel policy from the Trump Administration ? Bean and oil spreads firmed while meal spreads weakened. Spot board crush margins improved $.02 to $1.28 ½ bu. while bean oil PV exploded out to 46.2%, a 2 ½ year high. July-25 beans broke out to a 2 month high. Fresh 2 week low for July-25 meal. Spot oil jumped out to its highest level in 1 year on the weekly chart. Nearby futures have not been above $.50 lbs since Dec-23. Midday comments from Pres. Trump that his Administration did have trade discussions with China this morning helped stimulate late day strength. No results from today’s discussion are known at this time, however it sounds likely that communication lines between the Trump Administration and Beijing are being opened. Treasury yields fell on increased optimism the Fed will resume cutting rates soon helped fuel continued strength in the US equity markets. Bean exports at 10 mil. bu. were at the low end of expectations. YTD sales at 1.729 bil. are up 13% from YA vs. the USDA forecast of up 8%. Commitments represent 95% of the USDA forecast, in line with the historical average. No new sales to China. Outstanding sales to China/unknown slipped 1 mil. to 67 mil. Soybean meal sales at 176k tons were at the low end of expectations. YTD commitments are up 9% from YA, vs. USDA up 8%. Soybean oil sales at 12k mt (27 mil. lbs.) were in line with expectations. YTD commitments at 2.134 bil. lbs. represent 93% of the USDA forecast of 2.30 bil. lbs. Speculative traders are pretty much flat in the soybean complex, long 33k contracts of soybeans, 45k contracts of oil and short 77k contracts of meal. The BAGE kept their Argentine production forecast unchanged at 48.6 mmt, just below the USDA forecast of 49 mmt. Harvest advanced nearly 10% to 14.5% complete.

WHEAT

Prices recovered late to close steady to $.01 higher across the 3 classes. Spreads weakened in KC futures. New contract lows for KC futures with the spot contract falling to its lowest level since Dec-24. Next support is at $5.20. July-25 CGO and MGEX have both slipped to fresh 2 week lows before recovering late. Pres. Trump made a direct appeal to Russian Pres. Putin to shop the attacks on Ukraine now and to agree to a peace deal. This came in response to Russia’s deadliest assault this year on Ukraine’s capital of Kyiv that killed 12 and injured 90 other. Exports at 9 mil. bu. (-5 mil. – 24/25, 14 – 25/26) were in line with expectations. Old crop commitments slipped to 782 mil. bu. up 13% from YA, vs. the USDA forecast of up 16%. Shipments are up 11%. By class commitments vs. USDA: HRW +48% vs. USDA +53%, SRW -27% vs. -24%, HRS +4.5% vs. +8.5%, and white +44% vs. +45%. The market is clearly discounting higher crop ratings and production prospects as rains are expected to bring additional drought relief to the southern plains. Speculators remain heavily short in wheat with seemingly little fear of a price rally. Some day that will change, unlikely in the near-term.

Charts provided by QST.

>>See more market commentary here.

Risk Warning: Investments in Equities, Contracts for Difference (CFDs) in any instrument, Futures, Options, Derivatives and Foreign Exchange can fluctuate in value. Investors should therefore be aware that they may not realise the initial amount invested and may incur additional liabilities. These investments may be subject to above average financial risk of loss. Investors should consider their financial circumstances, investment experience and if it is appropriate to invest. If necessary, seek independent financial advice.

ADM Investor Services International Limited, registered in England No. 2547805, is authorised and regulated by the Financial Conduct Authority [FRN 148474] and is a member of the London Stock Exchange. Registered office: 3rd Floor, The Minster Building, 21 Mincing Lane, London EC3R 7AG.

A subsidiary of Archer Daniels Midland Company.

© 2021 ADM Investor Services International Limited.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.