Written Commentary

CORN

Prices finished steady to a penny lower in volatile trade. Spreads were mixed. The Goldman roll will be next week. July-25 didn’t seriously challenge the lows from earlier this week while overhead resistance remains at the 100 day MA at $4.72 ½. Old crop exports at 46 mil. bu. were in line with expectations. YTD commitments at 2.135 bil. are up 24% from YA, vs. the USDA forecast of up 7%. Current commitments represent 87% of the USDA forecast, above the historical average of 81%. Noted buyers were Korea – 13 mil., Mexico – 9 mil. and Taiwan with 6.5 mil. Pace analysis would suggest a higher export forecast than the current 2.45 bil. bu. however tariffs continue to cloudy up the picture. Reciprocal tariffs of 24% on imports from Japan and 25% from S. Korea will likely impact demand to our 2nd and 4th largest buyers of corn. While both Mexico and Canada were both exempt from additional tariffs, imports are still subject to the 25% fentanyl tariffs unless compliant with UMCCA guidelines. US corn area in drought fell another 5% in the past week to 39%, the lowest since last Oct. Census exports in Feb-25 at 238 mil. bu. were nearly 19 mil. above the weekly inspections data. Cumulative exports thru the first 6 months of the MY have reached 1.208 bil. bu. up 28% from YA.

SOYBEANS

Prices finished mostly lower with beans down $.18-$.20. While July-25 beans gapped below its 100 day MA support, prices remained well above last month’s lows. Bean oil closed roughly 140 points lower settling near the midpoint of today’s range. Meal prices were steady to $1 higher, rejecting trade into new contract lows. Beans spreads were slightly firmer while product spreads weakened. The soybean complex will likely be most impacted by the reciprocal tariffs as the Trump Administration added 34% to imports from China taking tariffs on most products to 54%, with some targeted products even higher. Reciprocal tariffs are scheduled to start next Wed. April 9th. Brazil’s Ag. Ministry is claiming to be nearing an agreement to supply DDG’S to China, helping to fill their hi protein feed needs. Bean exports at 15 mil. bu. were at the low end of expectations. YTD commitments at 1.696 bil. are up 14% from YA vs. the USDA forecast of up 8%. Commitments represent 93% of the USDA forecast, in line with the historical average. Outstanding sales to China/unknown have slipped to 96 mil. vs. 59 mil. YA. US soybean area in drought fell another 3% to 33%, also the lowest since last Oct. Census exports in Feb-25 at 113 mil. bu. brought cumulative exports in the first 6 months of the MY to 1.415 bil. bu. up 8.6% from YA.

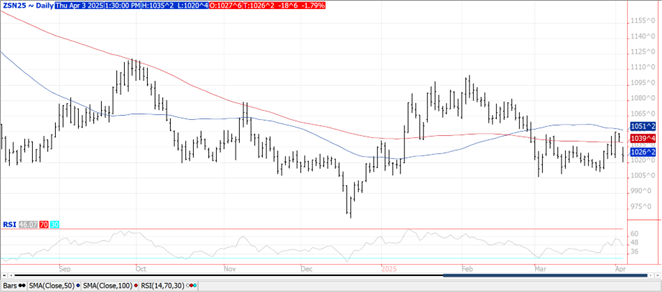

WHEAT

Prices were little changed closing mixed for the session. CGO and MGEX were $.01-$.03 lower while KC was up $.01. Exports at 16 mil. bu. (12.4 mil. – 24/25 MY, 3.5 – 25/26) were in line with expectations. Old crop commitments at 780 mil. bu. are up 13% from YA, vs. the USDA forecast of up 18%. By class commitments vs. USDA: HWW +47.5% vs. USDA +57%, SRW -28% vs. -24%, HRS +5% vs. +13%, and white +46% vs. +45%. The USDA attache to India expects their wheat production will reach a record 115 mmt in 2025, up from 113.3 mmt YA. US winter wheat area in drought slipped 1% LW to 37%, while spring wheat areas in drought held steady at 39%. Census exports in Feb-25 at 66 mil. bu. were nearly 9 mil. above the weekly inspections data. Cumulative exports thru the first 9 months of the MY have reached 590 mil. bu. up 20% from YA. In order to reach the USDA forecast, sales will need to reach 245 mil. the last Qtr. of the MY, well above the 208 mil. from YA.

Charts provided by QST.

>>See more market commentary here.

Risk Warning: Investments in Equities, Contracts for Difference (CFDs) in any instrument, Futures, Options, Derivatives and Foreign Exchange can fluctuate in value. Investors should therefore be aware that they may not realise the initial amount invested and may incur additional liabilities. These investments may be subject to above average financial risk of loss. Investors should consider their financial circumstances, investment experience and if it is appropriate to invest. If necessary, seek independent financial advice.

ADM Investor Services International Limited, registered in England No. 2547805, is authorised and regulated by the Financial Conduct Authority [FRN 148474] and is a member of the London Stock Exchange. Registered office: 3rd Floor, The Minster Building, 21 Mincing Lane, London EC3R 7AG.

A subsidiary of Archer Daniels Midland Company.

© 2021 ADM Investor Services International Limited.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.