Written Commentary

SOYBEANS

Prices closed higher across the complex with several contracts closing at or near session highs. Beans were up $.05 – $.08, meal was $2 – $4 higher while oil was up 40 – 60. Bull spreading was also noted across the complex. Mch-24 beans made a fresh 7 month low before recovering. Key support lies just below today’s low at $11.75. Resistance is at last week’s high of $12.23. Mch-24 oil also fell to a new 8 month low before recovering. Support is at its contract low 44.49 from last May-23. Resistance for Mch-24 meal is at last week’s high of $370.40. Weather concerns in Argentina remain elevated as extreme heat and limited rainfall this weekend kept stress levels high. Temperatures are expected to remain well above normal with very scattered showers thru mid-week. Better prospects for beneficial rains toward the end of this week and weekend which was reinforced with midday forecasts. Even with healthy rains next week, top end yield potential has likely been compromised. Conditions in Brazil are mostly favorable however dryness concerns are building in the interior south. Export inspections at 52 mil. bu. were well above expectations and the pace needed to reach the USDA export forecast of 1.755 bil. bu. YTD inspections at 1.070 bil. are down 24% from YA, vs. the USDA forecast of down 12%. AgRural estimates the Brazilian soybean crop is 16% harvested, vs. 9% from YA and 5-year Ave. of 10%. Last week MM’s were net sellers of just over 16k contracts of soybeans, 3k meal, and nearly 10k contracts of bean oil. Their combined short position in the soybean complex has swelled to nearly 185k contracts, the largest since May-2019.

CORN

Prices were mixed with old crop contracts within $.01 of unchanged while new crop futures were up $.01. Support for spot Mch-24 rests at the contract low of $4.36 ½ with resistance at last week’s high of $4.53 ¼. Export inspections at 25 mil. bu. were below expectations and well below the pace needed to reach the USDA export forecast of 2.10 bil. bu. YTD inspections at 641 mil. bu. are up 30% from YA, vs. the USDA forecast of up 26%. The USDA did announce the sale of 155k tons (6 mil. bu.) of corn to Mexico. AgRural est. Brazilian corn plantings in the center south region have reached 27%. Last week Money managers were net sellers of nearly 15k contracts, extending their short position in corn to 280k, the largest since June-2020 and within 42k of their record short position. Index funds have been net buyers of corn 4 out of the past 5 weeks while seeing their long position jump 60k contracts to nearly 272k.

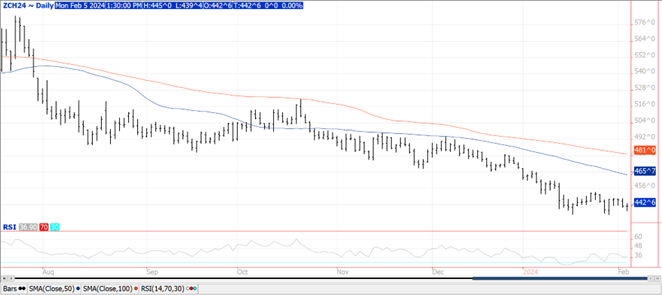

WHEAT

Prices were $.08 – $.11 lower across all 3 classes today, however spot Mch-24 contracts all held above last week’s low. As expected, good rains fell along the US southern plains, gulf coast and delta regions this weekend cutting into drought areas while building moisture reserves for the US winter wheat crop. IKAR reports Russian export prices finished last week at $228/mt on a FOB basis, down $7 from the previous week. SovEcon reports Russia exported 1.3 mmt of grain last week, up from only 830k mt the previous week. Wheat accounted for just over 1 mmt of those grain sales. Ukraine indicates that since Aug-23 they have been able to ship just over 20 mmt of cargo along the “Humanitarian Corridor”. Of this total just over 14 mmt were agricultural goods. Shipments in Jan-24 at 6.3 mmt nearly reached pre-war levels. US export inspections at 10 mil. bu. were in line with expectations however below the 15 mil. bu. needed per week to reach the USDA export forecast. Last week MM’s were net buyers of nearly 5k KC wheat, 3,200 MGEX wheat, and net sellers of 277 contracts of Chicago.

See more market commentary here.

Risk Warning: Investments in Equities, Contracts for Difference (CFDs) in any instrument, Futures, Options, Derivatives and Foreign Exchange can fluctuate in value. Investors should therefore be aware that they may not realise the initial amount invested and may incur additional liabilities. These investments may be subject to above average financial risk of loss. Investors should consider their financial circumstances, investment experience and if it is appropriate to invest. If necessary, seek independent financial advice.

ADM Investor Services International Limited, registered in England No. 2547805, is authorised and regulated by the Financial Conduct Authority [FRN 148474] and is a member of the London Stock Exchange. Registered office: 3rd Floor, The Minster Building, 21 Mincing Lane, London EC3R 7AG.

A subsidiary of Archer Daniels Midland Company.

© 2021 ADM Investor Services International Limited.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.