Written Commentary

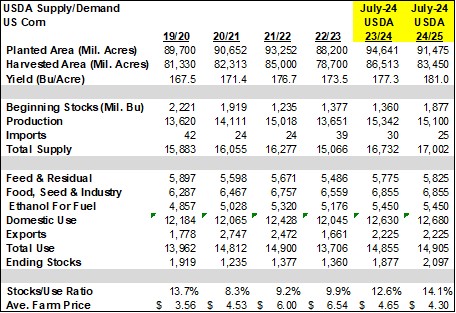

CORN

Old crop 23/24 ending stocks were cut 145 mil. bu. to 1.877 bil. as feed usage and exports were both raised 75 mil. bu. Stocks were 165 mil. below expectations and below the range of guesses. 2024 production at 15.10 bil. was in line with expectations following the higher acreage data from June. As expected no change to the record US yield forecast at 181 bpa. New crop usage was raised 100 mil. bu. with feed usage also up 75 mil and exports up 25 mil. despite the historically slow start. New crop ending stocks at just below 2.10 bil. were well below the average trade est. of 2.30 bil. Given the limited rebound in price, the markets seem skeptical of the USDA usage figures while also anticipating bigger yields down the road. Global stocks were revised up 1 mmt to 311.6 mmt, in line with expectations. Argentine production was cut 1 mmt to 52 mmt with exports also down 1 mmt. Mexico’s production was trimmed .6 mmt while exports were revised up by .9 mmt. Ukraine’s exports were increased 2 mmt to 28 mmt. MM’s are now holding a record short position at just over 350k contracts

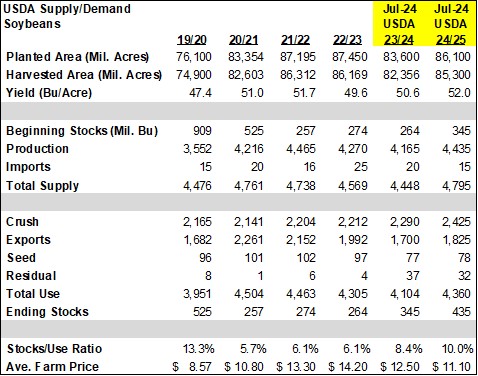

SOYBEANS

Old crop 23/24 ending stocks were cut 5 mil. bu. to 345 mil. as imports were cut 5 mil. Stocks were in line with expectations. 2024 production at 4.435 bil. was slightly above the Ave. trade est. of 4.415 bil. following the slightly lower acreage data from June. New crop usage left unchanged at 4.360 bil. leaving new crop ending stocks 435 mil. slightly below the average trade est. of 445 mil. Global stocks held steady at 128 mmt, in line with expectations. Argentine production was cut .5 mmt to 49.5 mmt while their exports were raised 1 mmt to 5.6 mmt. Surprisingly no change to the Brazilian production forecast as it held steady to 153 mmt. Their exports were also raised 1 mmt to 103 mmt. Near-term weather forecasts are non-threatening. By the end of the weekend temperatures are expected to build to the low 90’s for the central and ECB, upper 90’s to low 100’s for the WCB and plain states. By the middle of next week temperatures are expected to roll back to normal readings, at least for the northern half of the nation’s midsection. The net drying pattern over the next 5-7 days apparently isn’t concerning giving the historically low level of US cropland experiencing drought. This could change quickly and dramatically if the dryer pattern extends into late July.

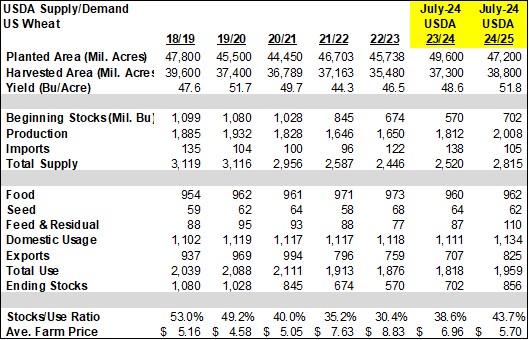

WHEAT

All wheat production at just over 2.0 bil. bu. was 95 mil. above expectations and above the range of estimates. Winter wheat production at 1.341 bil. bu. was up 46 mil. from June and 25 mil. above the ave. estimate. It was very close to our pre-report forecast of 1.345 bil. By class production was HRW – 763 mil. up 37 mil, SRW 344 mil. up 2 mil. and white 234 mil. up 8 mil. Spring wheat production at 578 mil. was a whopping 53 mil. above expectations. The Ave. yield at 53.1 bpa is well above the 10-year high of 48.6 bpa in 2020. Wheat imports in 24/25 were cut 15 mil. while demand was revised up by 35 mil. (feed up 10, exports up 25) resulting in ending stocks growing to 856 mil. if realized a 5 year high. Global stocks rose 5 mmt to 257 mmt, vs. expectations of holding steady. No significant changes globally with most of the higher world supplies a result of higher US.

Charts provided by USDA Supply/Demand.

>>See more market commentary here.

Risk Warning: Investments in Equities, Contracts for Difference (CFDs) in any instrument, Futures, Options, Derivatives and Foreign Exchange can fluctuate in value. Investors should therefore be aware that they may not realise the initial amount invested and may incur additional liabilities. These investments may be subject to above average financial risk of loss. Investors should consider their financial circumstances, investment experience and if it is appropriate to invest. If necessary, seek independent financial advice.

ADM Investor Services International Limited, registered in England No. 2547805, is authorised and regulated by the Financial Conduct Authority [FRN 148474] and is a member of the London Stock Exchange. Registered office: 3rd Floor, The Minster Building, 21 Mincing Lane, London EC3R 7AG.

A subsidiary of Archer Daniels Midland Company.

© 2021 ADM Investor Services International Limited.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.