Written Commentary

CORN

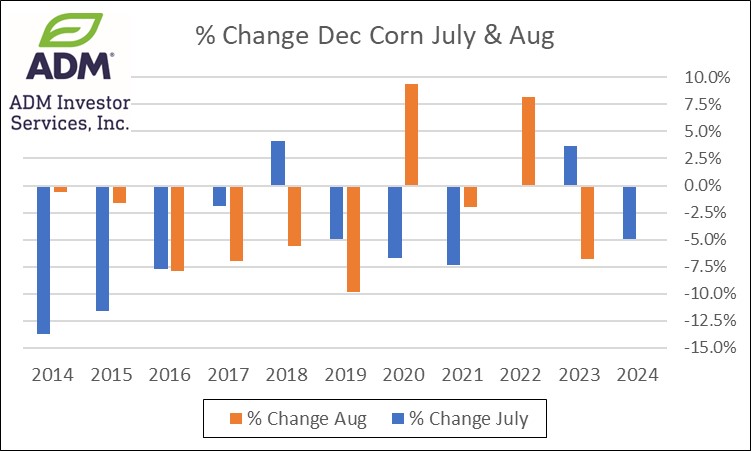

Prices were $.04-$.06 lower today with new contract lows for Sept-24 and the lowest spot price since Oct-2020 on the weekly chart. Dec-24 traded below $4.00 for the first time since Dec-20 however held just above its contract low at $3.95 ½. Spreads also traded out to new lows. The market wasn’t impressed with the 105k mt sale to an unknown buyer. Not even a record high weekly ethanol production figure could stimulate much of a price bounce. Production at 1,109 tbd last week was well above expectations and up 4% from YA. There was 111 mil. bu. of corn used, or 15.97 mil. bu. per day, above the 15.06 mbd needed to reach the USDA. Ethanol stocks jumped to 24 mil. barrels, a 10 week high, however were within the range of estimates. Implied gasoline usage last week fell 2.2% to 9.25 mbd, however was still up nearly 5% from YA. Dec-24 corn was down 5% for the month of July, closing below $4.00 for the first time since July-2020. Unfortunately recent history shows August hasn’t been a particularly good month for December corn as well, closing lower 8 of the past 10 years. Ukraine’s Ag. Minister cut their 2024 grain.

SOYBEANS

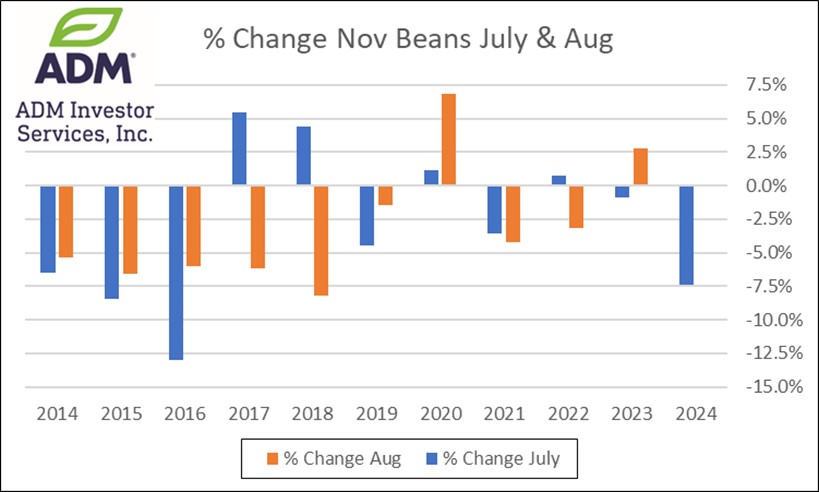

Prices recovered to close mixed. Beans were up $.01-$.03 ½ with new crop spreads all making new lows. Aug-24 beans carved out a new contract low at $10.20 ½ before recovering. Deliveries were modest at 44 contracts. Nov-24 traded to a fresh 3 ½ low before recovering. Spot oil quickly rejected trade below $.42 this week, much like it did this past May. Deliveries were in line with expectations at 936 contracts. As expected no deliveries against Aug-24 meal. Little change in US weather. Hot with only scattered rains for the central and southern plains. Rains will continue to favor the NC Midwest and ECB over the next 5-7 days as temperatures peak in the upper 80’s to low 90’s. By the 2nd week of August temperatures across the northern half of the Midwest are expected to dip to below normal readings with above normal precipitation across the nation’s midsection. Over a dozen US lawmakers wrote US Treasury Sec. Janet Yellen urging her agency to crack down on imported Used Cooking Oil (UCO) to ensure only domestic feedstocks can qualify for tax credits in the production of biofuels. Biodiesel and RD Capacity jumped 477 mil. gallons in May-24 to nearly 6.6 bil. gallons. This was the largest 1 month surge since Nov-22. Nearly all of the increase came from RD which is now pegged at 4.575 bil. gallons annually. BO usage in biodiesel and RD production increased slightly in May to 1.076 bil. lbs. As a feedstocks its usage rebounded to just over 37%, the highest since Sept-23 as prices responded to the drop to $.42 lbs this past spring. Total BO usage Oct-23 thru May-24 has reached 8.285 bil. lbs. up 9% from YA, vs. the USDA forecast of up 4%. Like corn, August has historically been a tough month for November soybeans as well closing down 8 of the last 10 year. Export sales tomorrow are expected to range from 15-44 mil. bu. for beans, 200-700k tons for meal and 0-15k tons for soybean oil.

WHEAT

After holding key support levels below the market prices recovered to closed mixed. Chicago finished $.03 higher, MGEX $.03 lower while KC was mixed. Cooler temperatures next week for the Canadian prairies however meaningful rain likely limited to SW regions. Hot/dry conditions to continue for E. Ukraine and S. Russia. Ukraine’s grain exports in July at 3.4 mmt were well above the 2.2 mmt from July-23. Their Ag. Ministries wheat production forecast at 19.8 mmt is still slightly above the USDA est. of 19.5 mmt. Favorable weather has raised Australia’s wheat production potential to as high as 30 mmt, up from 26 mmt YA and the current USDA 24/25 production est. of 29 mmt. Export sales tomorrow are expected to range from 8 – 22 mil. bu

Charts provided by QST Charts.

>>See more market commentary here.

Risk Warning: Investments in Equities, Contracts for Difference (CFDs) in any instrument, Futures, Options, Derivatives and Foreign Exchange can fluctuate in value. Investors should therefore be aware that they may not realise the initial amount invested and may incur additional liabilities. These investments may be subject to above average financial risk of loss. Investors should consider their financial circumstances, investment experience and if it is appropriate to invest. If necessary, seek independent financial advice.

ADM Investor Services International Limited, registered in England No. 2547805, is authorised and regulated by the Financial Conduct Authority [FRN 148474] and is a member of the London Stock Exchange. Registered office: 3rd Floor, The Minster Building, 21 Mincing Lane, London EC3R 7AG.

A subsidiary of Archer Daniels Midland Company.

© 2021 ADM Investor Services International Limited.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.