Written Commentary

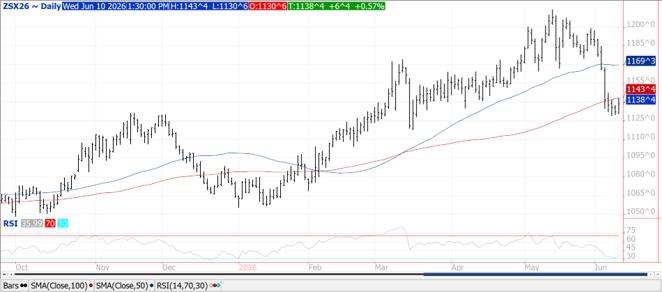

CORN

Prices ranged from $.00 ½ lower to were $.02 higher while spreads weakened. Support for July-26 is near $4.05 with resistance at $4.41. Traders expect little change in corn stocks and new crop production in tomorrow’s USDA updates. Ethanol production held steady at 1,108 tbd, or 326 mil. gallons last week, however was down 1% YOY. Production was slightly below expectations. There was 109 mil. bu. of corn used in the production process, or 15.5 mil. bu. per day, below the 16.0 needed to reach the USDA forecast of 5.60 bil. In the MY to date there has been 4.207 bil. bu. used, or 15.13 mbd, an annualized pace of 5.523 bil. Ethanol stocks slipped to 24.5 mil. barrels, above YA at 23.7 mb. Implied gasoline usage rose 1.6% to 8.731 tbd however was still 4.8% below YA. Conab will also update their Brazilian production forecasts tomorrow. Export sales tomorrow are expected to range from 35-70 mil. bu.

SOYBEANS

Prices were higher across the complex with beans up $.06-$.09, meal was steady to $1 higher while oil jumped 35-40 points. Bean and oil spreads firmed while meal spreads were mixed. Despite the strength, it was still an inside day for July-26 oil. Crush margins were off $.02 ½ to $3.70 bu. with bean oil PV improving to 55.5%. Energy prices were higher after US forces launched “self-defense strikes” against Iran in retaliation for downing a US helicopter a day earlier. Pres. Trump warned that Iran “must pay the price” for stalled peace negotiations while threatening to hit them “very hard” again today. After raising crush 20 mil. last month and lowering exports 10 mil. No changes expected for 2026 production or stocks. Still on the lookout for fresh Chinese demand interest in US soybeans. US FOB offers at the Gulf are steady with Brazil by Sept-26 while at a slight discount by Oct-26. Bean oil usage for biofuel production continues to play catch-up after the slow start to the 25/26 MY. Usage in Mch-26 at 1.283 bil. lbs. was a record high, however still needs to average 1.348 per month April through Sept. to reach the current USDA usage forecast of 14.2 bil. lbs. Monthly usage in 26/27 will need to average 1.483 bil. to reach the USDA’s 17.8 bil. lb. forecast. Surging D4 RIN values have kept biodiesel and RD margins profitable despite the higher BO cost. Under the current dynamics S&P Global calculates the B/E price for bean oil at $.93 lb. Anec raised their forecast for Brazilian exports in June-26 by 2 mmt to 14.4 mmt which if realized would be a record high for the month. Export sales are expected to range from 10-25 mil. bu. of soybeans, 300-600k mt of meal and 0-10k tons of soybean oil.

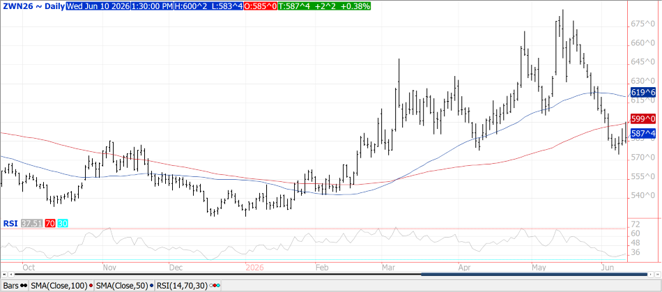

WHEAT

Prices were steady to $.03 higher closing $.09-$.15 off session highs across the 3 classes. Early strength was attributed to speculative buying as traders lighten up on recently established short positions while heavy rain across the S. Midwest threaten the winter crop just ahead of harvest. CGO July-26 was up $.02 ¼ at $5.87 ½ after briefly trading above the $6 level and its 100-day MA resistance at $5.99. KC July-26 traded to its highest level in a week before pulling back. MIAX July-26 traded to a 3 ½ month low. Also supporting wheat prices are reports from Ukraine’s largest farmer union UAC stating that damage to grain export terminals along the Black Sea from Russian missile attacks have been extensive and may threaten shipments of key agricultural goods. Export sales are expected to range from 5-20 mil. bu.

Risk Warning: Investments in Equities, Contracts for Difference (CFDs) in any instrument, Futures, Options, Derivatives and Foreign Exchange can fluctuate in value. Investors should therefore be aware that they may not realise the initial amount invested and may incur additional liabilities. These investments may be subject to above average financial risk of loss. Investors should consider their financial circumstances, investment experience and if it is appropriate to invest. If necessary, seek independent financial advice.

ADM Investor Services International Limited, registered in England No. 2547805, is authorised and regulated by the Financial Conduct Authority [FRN 148474] and is a member of the London Stock Exchange. Registered office: 3rd Floor, The Minster Building, 21 Mincing Lane, London EC3R 7AG.

A subsidiary of Archer Daniels Midland Company.

© 2021 ADM Investor Services International Limited.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.