Written Commentary

CORN

Prices were steady to $.01 ½ higher as spreads firmed up. Major support for July-25 is at $4.26 ½, the Mch-25 low on the weekly bar chart. Initial support for Dec-25 is at $4.34 ¼ with secondary support at the contract low of $4.28. The USDA cut 2024/25 ending stocks 50 mil. to 1.365 bil., 25 mil. below expectations as exports were raised 50 mil. to 2.650 bil. The old crop stocks/use at 8.9% is at a 4 year low. China’s 2024/25 imports were cut 1 mmt to 7 mmt. No change to SA production forecasts. Lower old crop stocks carried right thru to 2025/26 with stocks also down 50 mil. to 1.750 bil., 40 mil. below expectations. 2025/26 global stocks down 2.6 mmt to 275.2 mmt. Weekly exports at 30 mil. bu. were at the low end of expectations. Old crop commitments at 2.596 bil. are up 26% from YA, vs. the revised USDA forecast of up 16%.

SOYBEANS

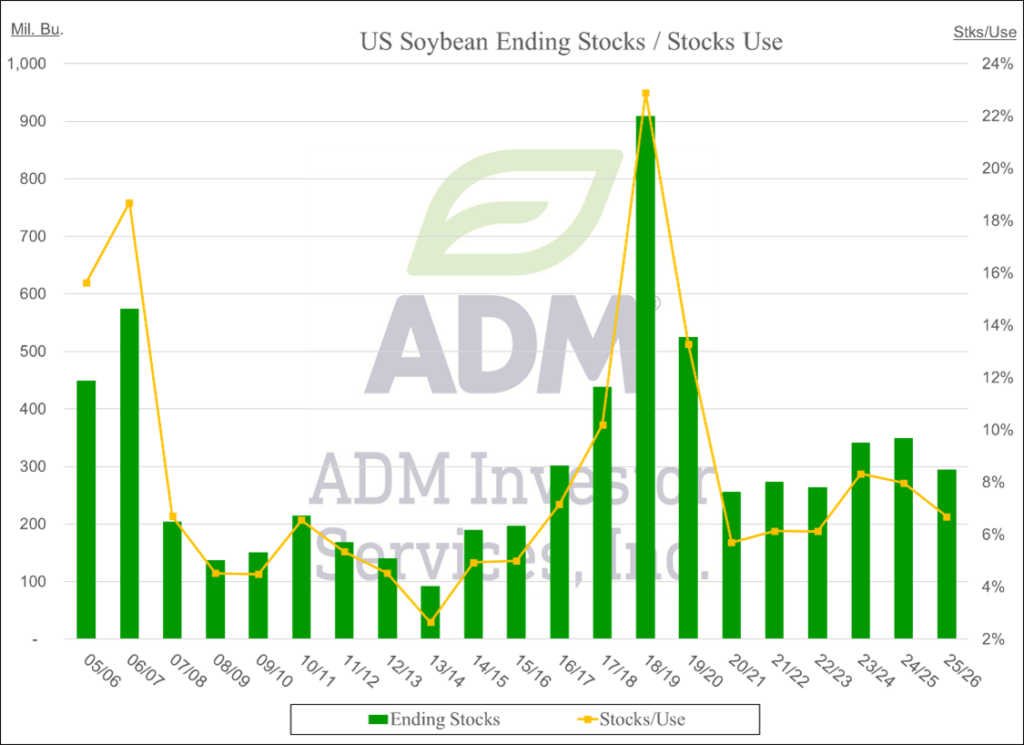

Prices were mostly lower with beans down $.02-$.08 led lower by spot July. Meal was fractionally higher while oil was off 30-40 points. Bean spreads remain under pressure after several Midwest processors switched their spot bids from the July contract to the new crop Nov futures, effectively dropping cash bids $.50-$.60 cents. July has slipped to a $.15 inverse over Nov-25, down $.15 from its recent peak. Next support for July futures is this month’s low of $10.32 ½ followed by the April low at $9.85. Huge range in July-25 oil today with prices closing moderately lower. Oil prices retreated as the Trump Administration is likely to propose lower quota’s than the 5.25 bil. gallons sought by the biofuels industry as they return to proposal to the EPA for further action. A mostly favorable weather outlook limits upside price potential for corn and soybeans. The USDA left 2024/25 US endings stocks unchanged at 350 mil. bu. in line with expectations. They did shift 200 mil. lbs. of bean oil demand from domestic biofuel usage to exports. China’s 2024/25 crush was cut 1 mmt to 108 mmt. US 2025/26 US ending stocks were also unchanged at 295 mil. bu. No changes to SA production forecasts. Global stocks were increased 1 mmt to 125.3 mmt. Soybean exports at 4 mil. bu., half old crop half new crop, were below expectations. Old crop commitments at 1.790 bil. are up 11% from YA vs. the USDA forecast of up 9%. No surprise the USDA export forecast was left unchanged. Soybean meal sales at 261k tons were in line with expectations. YTD commitments are up 12% from YA, vs. USDA up 8%. Soybean oil sales at 5.6k mt (12 mil. lbs.) were at the low end of expectations. YTD commitments at 2.322 bil. lbs. represent 89% of the revised USDA forecast of 2.60 bil. lbs. The BAGE pegs Argentine harvest at 93%, up 5% for the week. They raised their production forecast .3 mmt to 50.3 mmt above the USDA est. of 49 mmt.

WHEAT

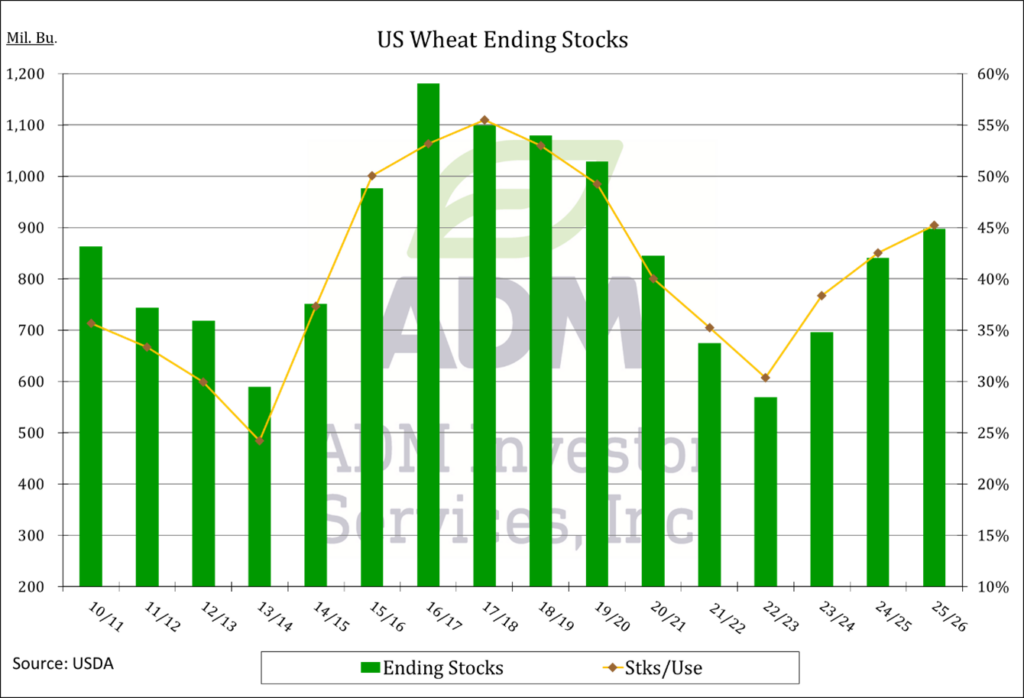

Prices ranged from $.07 lower in CGO to $.04 higher in MGEX. July-25 CGO and KC closed into new lows for the month. The USDA held 2024/25 ending stocks unchanged at 841 mil. bu. 2025 all wheat production was also unchanged at 1.921 bil. No surprise, WW production was also unchanged at 1.382 bil. 2025/26 ending stocks were cut 25 mil. to 898 mil. on higher exports. Despite the reduction, stocks are still up for a third consecutive year. Global stocks for 2025/26 were cut 3 mmt to 262.8 mmt. New wheat sales were less than 1 mil. bu. this week bringing new crop commitments at 217 mil. bu., an 8 year high, up 22% from YA, vs. the revised USDA forecast of up 1%. Commitments represent 26% of the USDA forecast, above the historical average of 20%. The BAGE reports planting progress advanced 15% LW to 38.5%.

Charts provided by QST.

>>See more market commentary here.

Risk Warning: Investments in Equities, Contracts for Difference (CFDs) in any instrument, Futures, Options, Derivatives and Foreign Exchange can fluctuate in value. Investors should therefore be aware that they may not realise the initial amount invested and may incur additional liabilities. These investments may be subject to above average financial risk of loss. Investors should consider their financial circumstances, investment experience and if it is appropriate to invest. If necessary, seek independent financial advice.

ADM Investor Services International Limited, registered in England No. 2547805, is authorised and regulated by the Financial Conduct Authority [FRN 148474] and is a member of the London Stock Exchange. Registered office: 3rd Floor, The Minster Building, 21 Mincing Lane, London EC3R 7AG.

A subsidiary of Archer Daniels Midland Company.

© 2021 ADM Investor Services International Limited.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.