Written Commentary

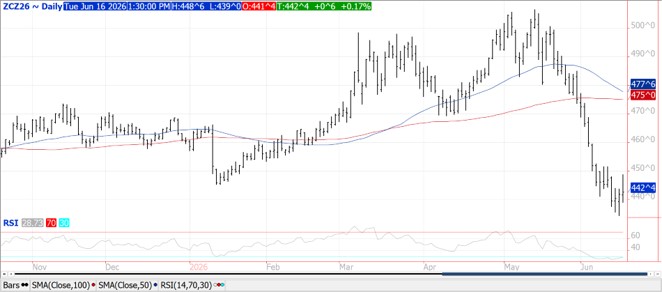

CORN

Prices were mixed while closing within $.02 of unchanged with bear spreading noted. July-26 rejected its first attempt at trading above $4.20 since last week’s USDA updates. Support is at $4.05, a gap on the weekly chart from last Sept-26. Corn ratings improved 1% to 68% G/E, in line with expectations as there was a 1% shift from fair to good. Ratings improved in 8 states while declining in 10. Overall ratings are historically average for mid-June. Emergence at 94% is in line with YA and the 5-year Ave. of 93%. S&P Global is forecasting 2026 corn acres reached 96 mil., up from their preplant est. of 95.2 mil. and above the USDA planting intentions in March at 95.34 mil. EU 25/26 corn imports as June 14th at 17.22 mmt are down 9.75% from YA. Tomorrow’s EIA report is expected to show ethanol production rebound to 330 mil. gallons up from 326 last week.

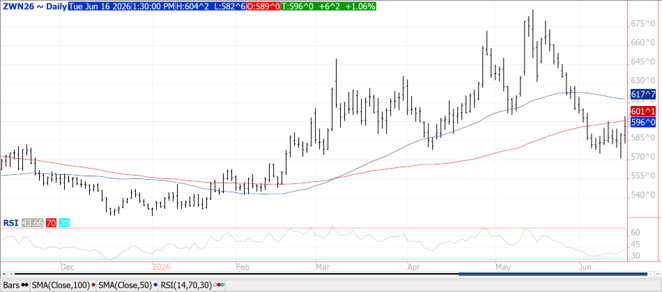

SOYBEANS

Prices were mixed with soybeans $.09-$.12 higher, meal was up $1-$2 higher while bean oil was down nearly $.01 ½ lbs. Bean and oil spreads weakened while meal spreads firmed. July and November beans both traded to a 2-week high with the Nov-26 contract closing right at its 100-day MA. Soybean prices flipped to close moderately higher on reports from cash connected sources that China’s Sinograin has inquired about US soybeans for late 2026, early 2027 shipment. As we mentioned in this AM comments US FOB offers have slipped to a slight discount to Brazil. July meal traded to a 4 ½ month low however held support above $300 before recovering. Despite the weakness, July oil held above yesterday’s low. Crush margins were pounded, down $.21 to $3.42 ½ with bean oil PV slipping to 54.5%. For now Chinese interest will likely be limited to state owned entities given the 10% reciprocal tariff on US imports. Plantings advanced 3% to 95% vs. the YA pace and 5-year Ave. of 93%. Emergence at 88% is above the 83% from YA and 5-year Ave. of 82%. Ratings improved 1% to 66% G/E. The ratings index improved to 81.8, slightly above the historical average. Oddly enough, ratings improved in only 6 states, declined in 11, while holding steady in 1. Ratings rose 7% in both IN and SD, while declining 8% in NE and down 7% in both LA and NC. EU soybean imports as of June 14th at 13.2 mmt are down 6% from YA. Their meal imports at 18.05 mmt are down 3.6%.

WHEAT

Prices range from $.06 lower in KC to $.06 higher in CGO. CGO July-26 briefly traded above $6.00 and its 100-day MA before closing at $5.96 up $.06 ¼. Early strength in KC July-26 fizzled out before challenging resistance at $6.45 while holding support at its 100-day MA. Winter wheat ratings rose 2% to 27% G/E vs. expectations of no change. 95% of the crop is headed vs. 92% YA and the 5-year Ave. of 91%. Harvest advanced more than expected to 25%, vs. only 9% YA and 5-year Ave. of 13%. There was a 1% decline in the crop rated poor/VP, down to 45%. Overall ratings are still the lowest in 20 years for mid-June. Spring wheat ratings improved another 3% to 55% G/E, slightly better than expected and are just below the 57% G/E from YA. Emergence at 95% is above YA at 88% and the 5-year Ave. of 89%. EU soft wheat imports as of June 14th at 22.4 mmt are up 7% YOY.

Risk Warning: Investments in Equities, Contracts for Difference (CFDs) in any instrument, Futures, Options, Derivatives and Foreign Exchange can fluctuate in value. Investors should therefore be aware that they may not realise the initial amount invested and may incur additional liabilities. These investments may be subject to above average financial risk of loss. Investors should consider their financial circumstances, investment experience and if it is appropriate to invest. If necessary, seek independent financial advice.

ADM Investor Services International Limited, registered in England No. 2547805, is authorised and regulated by the Financial Conduct Authority [FRN 148474] and is a member of the London Stock Exchange. Registered office: 3rd Floor, The Minster Building, 21 Mincing Lane, London EC3R 7AG.

A subsidiary of Archer Daniels Midland Company.

© 2021 ADM Investor Services International Limited.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.