Written Commentary

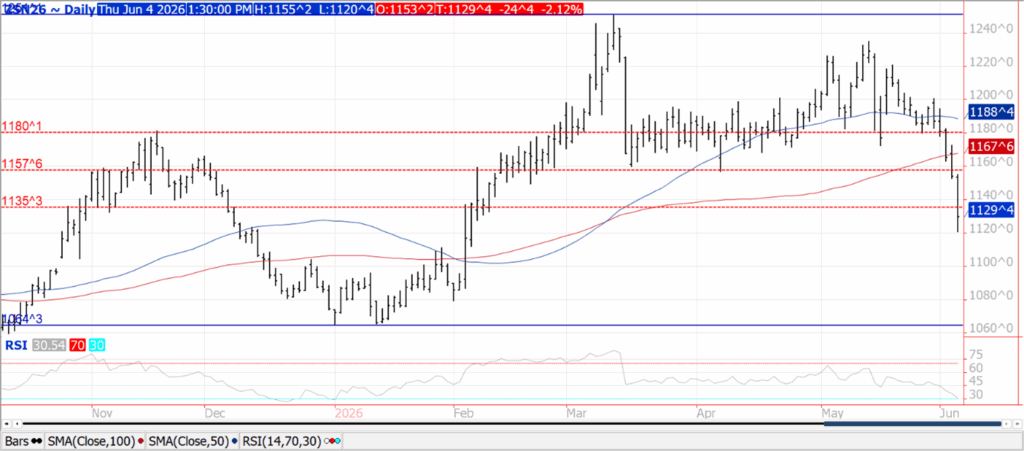

CORN

Prices were $.07-$.08 lower while spreads finished slightly firmer after trading to new lows early in the session. July-26 traded to a new contract low while Dec-26 fell to a 4 ½ month low. July also violated support at the 50 and 100-week MA average on the spot weekly chart. Next support is $4.17 ¼. Favorable US weather, weaker than expected export demand along with reports a calf in Texas tested positive for the New World screwworm have all weighed on agricultural commodities. Feed grain and protein demand may weaken if a widespread outbreak of the disease further tightens US cattle supplies. The Argentine Govt. outlined their plans to lower corn export taxes from the current 8.5% to 7.5% by the end of 2027, then to 5.5% in Dec-28. US export sales at 45 mil. bu. was at the low end of expectations. Old crop commitments at 3.219 bil. bu. are up 26% from YA, vs. the USDA forecast of up 15.5%. Japan bought 13 mil., Mexico 10 mil. while S. Korea bought 8 mil. Costa Rica bought nearly 5 mil. bu. of new crop. We are starting to see some building of new crop export commitments. At 126 mil. bu. they are the highest in 4 years, however remain historically low. The BAGE held their Argentine production forecast unchanged at 64 mmt, vs. the USDA est. at 59 mmt. Harvest advanced 6% to 41%.

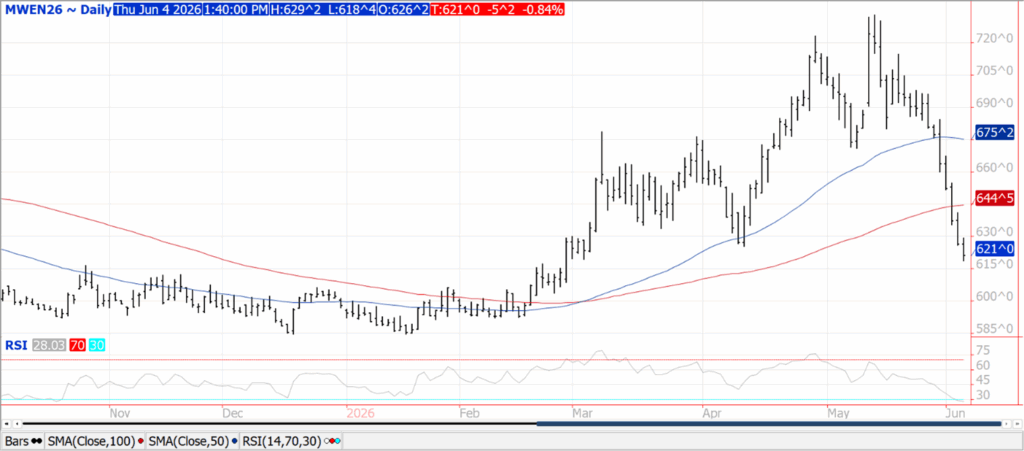

SOYBEANS

Prices were sharply lower across the complex with beans down $.24-$.27, meal was $6-$8 lower while oil is down over $.02 lb. Beans spreads were mixed while product spreads weakened. July-26 beans fell to a 4-month low while Nov-26 hit a 2-month low. Still waiting for renewed Chinese soybean interest. The US FOB offer premium to Brazil has slipped to $.20-$.30 bu. for July/Aug while pretty much even for Sept forward. This week’s high in July-26 oil was the highest in 4 years driven by surging RIN values and increased RD production margins. Board crush margins backed off $.17 ½ bu. from yesterday’s all-time closing high at $4.17 ½ bu. Bean oil PV rests near its all-time high at 55%. The American Fuel and Petrochemical Manufacturers trade group filed a lawsuit challenging the EPA biofuel mandates arguing they increase compliance costs and raise fuel prices. Argentina is lowering their current soybean export tax of 24% to 21% starting in Dec-27, then down to 15% starting in Dec-28. Soybean oil export taxes that currently range from 18-22% will fall to 11-14% by the end of 2028. US soybean exports at 19 mil. were below expectations. Old crop commitments at 1.468 bil. are down 18% from YA in line with the USDA forecast. Sales to China have reached 11.95 mmt with another 1.37 mmt to unknown. Shipments to China have reached 11.5 mmt. New crop commitments at only 33 mil. bu. are historically low. Meal sales at 232k tons were in line with expectations. Old crop commitments are up 16%, vs. the USDA forecast of up 8%. Bean oil sales were zippo leaving commitments at 823 mil. lbs. down 64% vs. USDA forecast of down 52%. The BAGE kept their Argentine production forecast unchanged at 50.1 mmt while harvest advanced 7% to 92%.

WHEAT

Prices ranged from $.04-$.07 lower across the 3 classes. CGO July-26 was down $.05 ½ at $5.81 ¾ while holding support above its April low of $5.77 ¾. KC July-26 was down $.03 ¾ at $6.20 ¼ while MIAX July-26 was $.05 ¼ lower at $6.21. Initial support for KC July-26 is at $6.12. MIAX July-26 is now $1.10 bu. off last month’s high. The price gap for US wheat and other global exporters has narrowed in recent weeks. Argentina’s tax cut on wheat exports from 7.5% to 5.5% is now in effect. This week saw major shifting of old crop sales to new crop as we wind down the 25/26 MY. Net sales at only 7 mil. bu. (-24 mil.–25/26 MY, 31 mil.–26/27) were also at the low end of expectations. Old crop commitments at 868 mil. bu. are up 11% from YA, vs. the USDA forecast of up 10%. Tunisia reportedly bought 75k mt of optional origin feed wheat at just over $268/mt CF for July/Aug shipment. Spring wheat acres in drought held steady at 23% while durum jumped 13% to 55%. The BAGE reports Argentine wheat plantings advanced 18% to 32%.

Risk Warning: Investments in Equities, Contracts for Difference (CFDs) in any instrument, Futures, Options, Derivatives and Foreign Exchange can fluctuate in value. Investors should therefore be aware that they may not realise the initial amount invested and may incur additional liabilities. These investments may be subject to above average financial risk of loss. Investors should consider their financial circumstances, investment experience and if it is appropriate to invest. If necessary, seek independent financial advice.

ADM Investor Services International Limited, registered in England No. 2547805, is authorised and regulated by the Financial Conduct Authority [FRN 148474] and is a member of the London Stock Exchange. Registered office: 3rd Floor, The Minster Building, 21 Mincing Lane, London EC3R 7AG.

A subsidiary of Archer Daniels Midland Company.

© 2021 ADM Investor Services International Limited.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.