Written Commentary

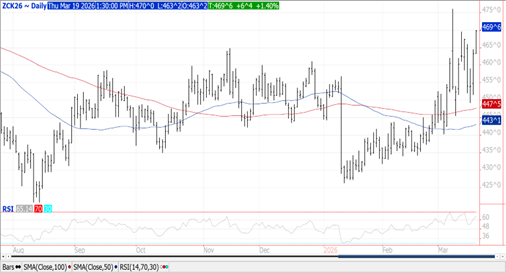

CORN

Prices are $.04-$.06 higher today while spreads firmed. Resistance for May-26 is at this month’s high of $4.76. I look for prices to hold in a $4.40-$4.80 range with energy likely to drive a directional breakout. Dec-26 is holding just below this month’s high of $4.98 ½. Exports at 46 mil. bu. was in line with expectations and brought YTD commitments to 2.664 bil. bu. up 30% from YA, vs. the USDA forecast of up 15.5%. Commitments represent 81% of the USDA forecast, above the historical average of 75%. Noted buyers were Mexico – 11 mil., Japan – 8 mil. and Spain – 6 mil. COF after tomorrow’s close is expected to show cattle at 99% of YA levels. The International Grains Council (IGC) forecasts global corn production in 2026/27 MY at 1.30 bil. Mt, down from 1.32 bil. Mt in 25/26. The BAGE placed Argentina corn harvest at 13% while holding production at 57 mmt, well above the USDA est. of 52 mmt. 90% of the crop is rated normal-excellent.

SOYBEANS

Prices were mostly higher with beans up $.05-$.07, meal surged $7-$11 while oil slipped 15-20 points. May-26 meal surged to its highest level since early Dec-25 with strength being attributed to a potential Brazilian port workers strike while Argentina has been less than aggressive in offering new crop supplies for export. Also rumors that the Trump Administration may not announce final RVO and SRE policies at next Friday’s Agricultural event at the White House triggered some buy meal, sell oil spreading. China reportedly rejected another Brazilian cargo yesterday due to pests. Spot board crush margins surged another $.15 ½ bu. to a fresh 3 ½ year high at $2.82 ½ with bean oil PV slipping to 49.6%. With US crush rates at record highs, look for another 10-20 mil. bu. increase to the current USDA crush forecast of 2.575 bil. bu. Export sales at 11 mil. were below expectations. YTD commitments at 1.352 bil. are down 19% from YA vs. the USDA forecast of down 16%. Sales to China at 80k mt (66k switched from unknown) bring total commitments to 11 mmt with another 2.0 mmt parked in unknown. Shipments to China are nearly 7.9 mmt. Meal sales at 221k tons bring YTD commitments to 12,394k tons up 11% YOY vs. the USDA up 5%. Bean oil sales at 11.5 mil. lbs. brought commitments to 796 mil. lbs. down 58% YOY vs. USDA forecast of down 52%. Without additional sales to China the USDA export forecast is too high. The Trump Admin. Is looking to firm up dates for Trump’s trip to Beijing. Abiove raised their Brazilian production forecast .7 mmt to 177.85 mmt, compared to the USDA est. of 180. They kept their export forecast unchanged at 111.5 mmt vs. the USDA est. of 114. They raised their crush est. .5 mmt to 61.5 mmt, just above the USDA at 61. The BAGE held their production forecast unchanged at 48.5 mmt, vs. USDA at 48 mmt.

WHEAT

A late recovery in KC futures enabled prices to close higher across all 3 classes ranging from $.03 higher in KC to $.07 higher in MIAX. Spreads were steady to weaker. Today is the 1st day the VSR for SRW wheat dips to $00165 per day. CGO May-26 for now rejected trade into new highs for the week. Next resistance for May-26 KC is this month’s high of $6.47 ½. Big temperature swings and growing drought in the SW plains should provide underlying support. Potential rains 10 days out should not be viewed with a great deal of confidence just yet. The recent price surge has left US wheat less competitive in the global marketplace, which should work to cap prices below their recent highs. Export sales at only 7 mil. bu. was below expectations while bringing YTD commitments to 870 mil. bu. up 14% from YA, vs. the USDA forecast of up 9%. Commitments represent 97% of the USDA forecast, above the historical average of 92%.

Charts provided by CQG

Risk Warning: Investments in Equities, Contracts for Difference (CFDs) in any instrument, Futures, Options, Derivatives and Foreign Exchange can fluctuate in value. Investors should therefore be aware that they may not realise the initial amount invested and may incur additional liabilities. These investments may be subject to above average financial risk of loss. Investors should consider their financial circumstances, investment experience and if it is appropriate to invest. If necessary, seek independent financial advice.

ADM Investor Services International Limited, registered in England No. 2547805, is authorised and regulated by the Financial Conduct Authority [FRN 148474] and is a member of the London Stock Exchange. Registered office: 3rd Floor, The Minster Building, 21 Mincing Lane, London EC3R 7AG.

A subsidiary of Archer Daniels Midland Company.

© 2021 ADM Investor Services International Limited.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.