Written Commentary

CORN

Prices ranged from $.01-$.02 lower in old crop to $.03 ½ higher in new crop. Disappointing trade in old crop corn given the tighter than expect stocks. New crop spreads firmed up a bit. Prices shot up to fresh session highs shortly after the release of the USDA reports however quickly backed off as favorable US weather limits the upside. Old crop 24/25 ending stocks were cut 50 mil. bu. to 1.415 bil. on higher exports, 30 mil. below expectations. Brazil 2024/25 production rose 4 mmt to 130 mmt. Their domestic usage rose 3 mmt to 91 mmt as usage for ethanol production continues to expand. Their exports were cut 1 mmt resulting in stocks doubling to 6 mmt. 2025 US production is forecast at a record 15.820 bil. bu. slightly above expectations. Trendline yields were left at 181 bu. per acre, unchanged from the Feb-25 Outlook. New crop 25/26 ending stocks forecast to rise to only 1.80 bil. bu. more than 200 mil. below expectations. New crop usage is forecast at a record 15.460 bil. bu. The average US farm price for 25/26 forecast to fall to $4.20 bu. down from $4.35 in 24/25. Global stocks expected to drop nearly 10 mmt in 25/26 to 278 mmt nearly 20 mmt below expectations.

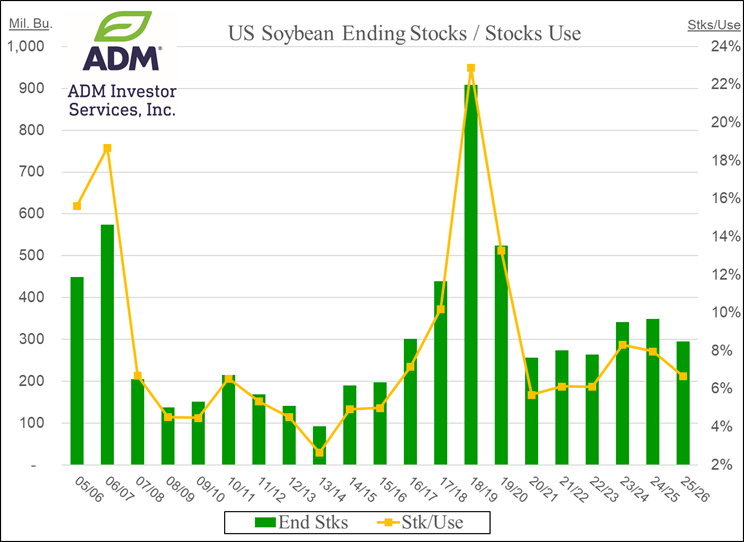

SOYBEANS

Prices were higher across the complex. Ahead of today’s USDA reports prices across the Ag. space were higher as US/Chinese trade negotiations this weekend in Geneva Switzerland were constructive. Both sides agreed to lower their reciprocal tariffs to 10%. The US will still impose a 20% import tariff on most goods for China’s alleged role in the US fentanyl crisis, effectively leaving tariffs on Chinese imports at 30%. A far cry away from the 145% heading into the weekend and well below the 80% Pres. Trump suggested just last Friday. This AM Pres. Trump said he expects to speak with Chinese leader Xi later this week. Beans ranged from $.20-$.27 better, meal was $4-$5 higher while oil was up 135 points. New crop futures were the upside leaders. Old crop 24/25 ending stocks were cut 25 mil. bu. to 350 mil. on higher exports, at the low end of expectations. Brazil’s exports and China’s imports for 2024/25 were cut 1 mmt. Bean oil usage for biofuels was cut 150 mil. lbs with exports up 100 mil. lbs, and imports down 50 mil. lbs. resulting in ending stocks unchanged at 1.531 bil. lbs. US production in 2025 is forecast at 4.340 bil. bu. in line with expectations. The average yield held at a record of 52.5 bpa. New crop 25/26 ending stocks forecast are forecast to fall to a 3 year low at 295 mil. bu. 65 mil. below expectations. The average US farm price is expected to rise to $10.25 per bu. up from $9.95 YA. Global stocks in 25/26 expected to increase to 124 mmt, 2 mmt below expectations. New crop soybeans likely has the most upside potential in the near term as the market will work to attract more acres. The US balance sheet could start looking pretty snug if record yields are not attained and Trump Administration is successful in negotiating a trade deal with China.

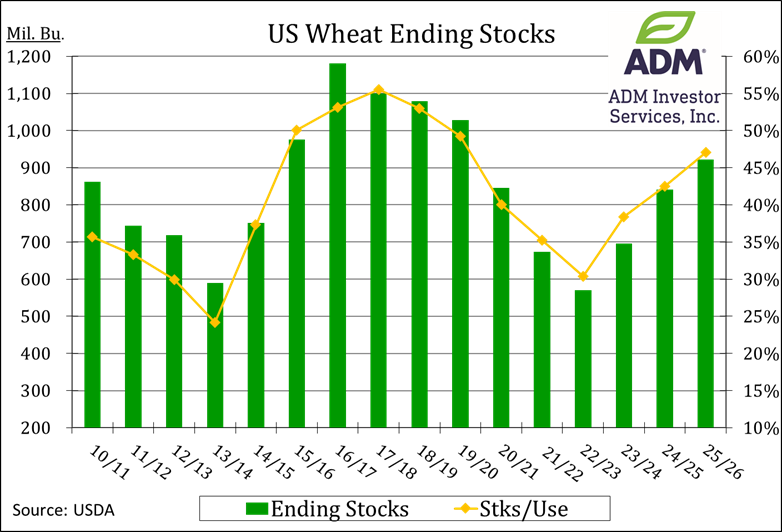

WHEAT

Prices range from $.06-$.10 lower across the 3 classes. Old crop 24/25 ending stocks were down 5 mil. bu. to 841 mil. on higher food usage at the low end of expectations. All wheat production for 2025 is forecast at 1.921 bil. 35 mil. above expectations. Winter wheat production at 1.382 bil. up 33 mil. from YA vs. expectations of down 25 mil. HRW production at 784 mil. was 35 mil. above expectations. SRW production at 345 mil. was in line, while white winter wheat production at 253 was also above expectations. 2025/26 ending stocks are forecast to rise to a 7 year high at 923 mil. bu., roughly 60 mil. above expectations. Global stocks for 25/26 are little changed from the previous year at 266 mmt, however above expectations. MGEX was pressured by forecasts for rain across the N. plains later this week following the record heat.

Charts provided by QST.

>>See more market commentary here.

Risk Warning: Investments in Equities, Contracts for Difference (CFDs) in any instrument, Futures, Options, Derivatives and Foreign Exchange can fluctuate in value. Investors should therefore be aware that they may not realise the initial amount invested and may incur additional liabilities. These investments may be subject to above average financial risk of loss. Investors should consider their financial circumstances, investment experience and if it is appropriate to invest. If necessary, seek independent financial advice.

ADM Investor Services International Limited, registered in England No. 2547805, is authorised and regulated by the Financial Conduct Authority [FRN 148474] and is a member of the London Stock Exchange. Registered office: 3rd Floor, The Minster Building, 21 Mincing Lane, London EC3R 7AG.

A subsidiary of Archer Daniels Midland Company.

© 2021 ADM Investor Services International Limited.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.