Written Commentary

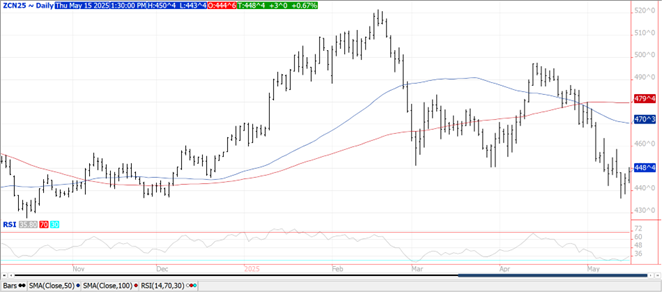

CORN

Prices ranged from $.03 higher in old crop to $.02 lower in new crop. Cumulative rains across the central Midwest thru the early half of next week are expected to bring widespread 1.5-3”, nearly ideal for the recently planted crops. Extended forecasts lay out a cooler than normal pattern in the east, warmer in the west with mostly normal precipitation across much central Midwest. July-25 jumped back out to a $.10 premium to Dec-25. Exports at 86 mil. bu. (66 mil. – 2024/25 MY, 20 – 25/26) were above expectations. Old crop commitments at 2.444 bil. are up 28% from YA, vs. the revised USDA forecast of up 13%. Current commitments represent 94% of the USDA forecast, above the historical average of 89%. Shipments are up 27%. Noted buyers were Korea – 24 mil., Mexico – 12 mil. and Japan – 8 mil. Conab raised their Brazilian production forecast 2.2 mmt to 126.9 mmt, still below the updated USDA forecast of 130 mmt. Algeria reportedly passed on their recent tender for 320k mt of corn however sources suggest they may have bought a much smaller volume from SA source. US corn acres in drought rose 2% this past week to 22%, well below last fall’s peak at 81%.

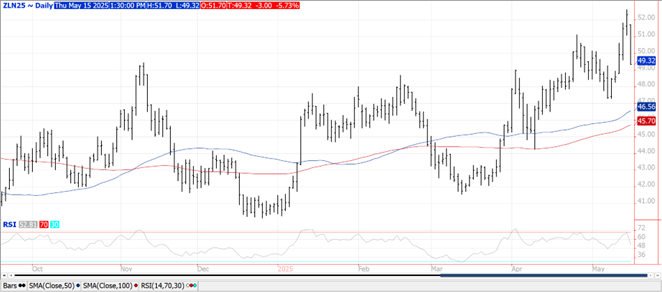

SOYBEANS

Prices were sharply mixed with beans down $.25-$.27. July-25 beans bottomed out at its 100 day MA support. The first 9 contracts of bean oil were locked limit down. Spreads would suggest spot July-25 was down another 80-90 points. Meal was $4-$5 higher. Comments from EPA Administrator Lee Zeldin that a legislative decision on biofuel tax credits and blending mandates could take months sent prices falling overnight. Unconfirmed rumors the volume recommendation may fall well short market expectations sent futures down the daily limit. The recent price jump in bean oil was largely driven by speculation the Trump Administration would quickly approve legislation on tax credits and blending volumes. Current production capacity for biodiesel and RD is just over 6.5 bil. gallons annually with proposed mandates well short of this level. After reach a 2 ½ year high yesterday at 47.3%, bean oil PV plunged to 45.4%, even lower when you consider the synthetic price. Soybean exports at 28 mil. bu. were in line with expectations. Old crop commitments at 1.764 bil. are up 13% from YA vs. the revised USDA forecast of up 9%. Shipments are up 12%. Soybean meal sales at 320k tons were in line with expectations. YTD commitments are up 9% from YA, vs. USDA up 8%. Soybean oil sales at 13.6k mt (30 mil. lbs.) were in line with expectations. YTD commitments at 2.214 bil. lbs. represent 92% of the revised USDA forecast of 2.40 bil. lbs. Conab raised their Brazilian production forecast .4 mmt to 168.3 mmt, a touch below the USDA forecast of 169 mmt. US bean acres in drought rose 2% to 17%. NOPA crush in April-25 at 190.2 mil. bu. was above expectations of 184 mil. and at the very high end of the range of guesses. Bean oil stocks rose to 1.527 bil. lbs. roughly 80 mil. lbs. above expectations. Implied census crush at 202 mil. bu. would bring YTD crush to 1.641 bil. bu. up 5.8% YOY, in line with the current USDA forecast.

WHEAT

Prices closed higher across all 3 classes with KC and CGO up $.05-$.08 while MGEX was up $.03. The recent selloff has brought out global buyers. Algeria reportedly bought 660k mt in their recent tender largely from the Black Sea region paying roughly $244.50/mt CF. Saudi Arabia’s food security agency is seeking 655k mt of wheat in a tender that expires tomorrow. Results are expected next Mon. the 19th with shipment from Aug thru Oct. Conab lowered their 2025 Brazilian wheat production forecast .22 mmt to 8.25 mmt, vs. the USDA est. of 8 mmt. US exports at 29 mil. bu. were above expectations. Old crop commitments at 789 mil. bu. are up 14% from YA, vs. the USDA forecast of up 16%. Shipments are up 11%. The Kansas Wheat Quality Council crop tour ended today. They est. Kansas wheat production at 338.5 mil. bu. with an average yield of 53 bpa. While their yield was well above Monday’s USDA forecast of 50 bpa, their production forecast was below the USDA’s est. of 345 mil. suggesting they see harvested acres much lower.

Charts provided by QST.

>>See more market commentary here.

Risk Warning: Investments in Equities, Contracts for Difference (CFDs) in any instrument, Futures, Options, Derivatives and Foreign Exchange can fluctuate in value. Investors should therefore be aware that they may not realise the initial amount invested and may incur additional liabilities. These investments may be subject to above average financial risk of loss. Investors should consider their financial circumstances, investment experience and if it is appropriate to invest. If necessary, seek independent financial advice.

ADM Investor Services International Limited, registered in England No. 2547805, is authorised and regulated by the Financial Conduct Authority [FRN 148474] and is a member of the London Stock Exchange. Registered office: 3rd Floor, The Minster Building, 21 Mincing Lane, London EC3R 7AG.

A subsidiary of Archer Daniels Midland Company.

© 2021 ADM Investor Services International Limited.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.