Written Commentary

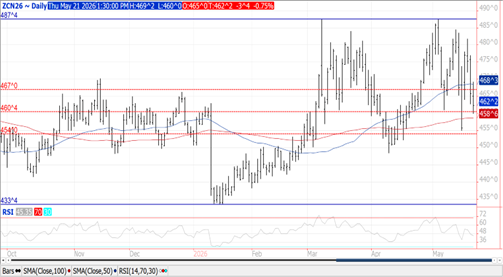

CORN

Prices were $.03-$.04 lower in 2-sided trade. Spreads were slightly firmer. July-26 held support near its 50% retracement between the January low and the double top at $4.87 ½. While yesterday’s EIA data showed ethanol production improved from the previous week, it was below the pace needed to reach the USDA corn usage est. for a 5th consecutive week. No date has been set for the US Senate to vote on E-15. Friday’s COF report is expected to show cattle inventories as of May 1st at 11.536 mil. head, up 1.4% from YA. Placements are expected to rise 3% with marketings down 9.5%. Prospects for sales to China have raised the price floor for corn while favorable weather limits the upside. Near-term look for July-26 to hold in a $4.50-$4.90 range. Exports at 95 mil. bu. were above expectations with old crop sales at a 4-month high. YTD commitments at 3.144 bil. bu. is up 26% from YA, vs. the USDA forecast of up 15.5%. Japan bought 31 mil., S. Korea 18 mil. while Mexico bought 13.5 mil. of old crop and 11 mil. bu. of new. New crop commitments at only 92 mil. bu. are the lowest for mid-May this decade. The BAGE raised their Argentine production forecast 3 mmt to 64 mmt, once again forging a gap with the USDA forecast of 59 mmt.

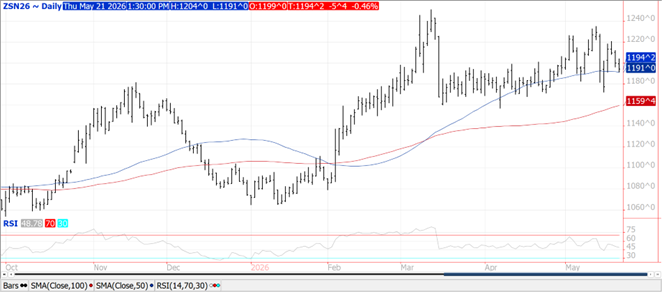

SOYBEANS

Lower trade across the complex with beans down $.05-$.06, meal was off $2-$3 while oil was 60-80 points lower. Bean spreads firmed, meal spreads were mixed while oil spreads weakened. July-26 beans bounced off its 50-day MA overnight at $11.91. MA support for Nov-26 is at $11.64 ¼. Prices across the Ag. space drifted lower into the close, largely in tandem with the reversal in energy prices. Spot WTI crude oil went from trading $4 per barrel higher to down $2.50 at it low. The reversal in energy prices likely due to reports from Iran News Agency that US/Iran have reached a peace agreement through intermediaries in Pakistan. Confirmation of a peace agreement however is lacking. Crush margins backed up another $.08 ½ to $3.41 bu. while bean oil PV slipped just under 53%. US Gulf FOB offer premium over Brazilian soybeans is down to $.35 bu. for Sept-26 shipment, while still more than $1 over Argentine offers. Near record high crush margins to fuel expanding biofuel production along with the potential for Chinese demand to return to pre-tariff levels has raised the price floor while favorable weather limits the upside. Soybean exports at 21 mil. were toward the high end of expectations. Old crop commitments at 1.447 bil. are down 18% from YA in line with the USDA. Sales to China have reached 11.87 mmt with another 1.38 mmt to unknown. Shipments to China have reached 11.2 mmt. Meal sales at 476k tons were in line with expectations and brought YTD to up 18% vs. the USDA up 8%. Bean oil sales at 2 mil. lbs. brought commitments to 814 mil. lbs. down 64%, vs. USDA forecast of down 52%. New crop soybean commitments at only 19 mil. bu. are at their slowest pace this decade. The BAGE raised their Argentine production forecast 1.5 mmt to 50.1 mmt, above the USDA est. of 48 mmt. Biodiesel blending credits (D4 RIN’s) totaled 690 mil. in April, up 5.7% from March and are the highest since Dec-24.

WHEAT

Prices ranged from $.04 to $.13 lower across the 3 classes. CGO July-26 was down $.13 at $6.47 ½, KC July-26 was off $.11 ¾ at $6.87 while MIAX July-26 was down $.04 ¼ at $6.90 ¼. CGO July-26 spread over July-26 corn has backed up $.09 ½ to $1.85, $.20 off its recent high. It would appear wheat is least likely to benefit from the Chinese trade agreement with US prices uncompetitive in the global marketplace. The Illinois Wheat Association 1 day crop tour projected an average yield of 102.8 bpa, just below YA results of 106 bpa. Their findings are well above the official 2026 USDA forecasts last week at 84 bpa, which was just below last year’s record yield of 88 bpa. Exports at 11 mil. bu. were in line with expectations. Old crop commitments at 921 mil. bu. are up 17% from YA, vs. the USDA forecast of up 10%. Commitments represent 101% of the USDA forecast, above the historical average of 97%. The IGC lowered their 26/27 global production forecast 1 mmt to 820 mmt, in line with the USDA’s 819 mmt est.

Risk Warning: Investments in Equities, Contracts for Difference (CFDs) in any instrument, Futures, Options, Derivatives and Foreign Exchange can fluctuate in value. Investors should therefore be aware that they may not realise the initial amount invested and may incur additional liabilities. These investments may be subject to above average financial risk of loss. Investors should consider their financial circumstances, investment experience and if it is appropriate to invest. If necessary, seek independent financial advice.

ADM Investor Services International Limited, registered in England No. 2547805, is authorised and regulated by the Financial Conduct Authority [FRN 148474] and is a member of the London Stock Exchange. Registered office: 3rd Floor, The Minster Building, 21 Mincing Lane, London EC3R 7AG.

A subsidiary of Archer Daniels Midland Company.

© 2021 ADM Investor Services International Limited.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.