Written Commentary

CORN

Prices were $.02-$.03 higher in 2 sided trade. Spreads were mixed with today being day 3 of the Goldman roll. Dec-25 continues to consolidate around the $4.30 level. Near term resistance is at the October high of $4.37 with support at the 100 day MA at $4.19 ¼. As trade talks continue, Thailand has agreed to cut corn import tariffs to zero while pledging to increase US corn imports between Feb-26 thru June-26 to 1.0 mmt, up from a previous quota of just under 55k mt. EU 25/26 corn imports as of Nov. 9th at 5.6 mmt are down 25.5% YOY. A Rueter’s survey shows traders expect lower US corn and soybean production on Friday. The Ave. corn production est. at 16.557 bil. bu. is down 257 mil. bu. from the USDA est. in Sept-25 and about 120 mil. bu. above our est. The Ave. yield is expected to slip to 184 bpa, while still a record it would be down from the 186.7 USDA est. in Sept. Despite the lower production US endings stocks are expected to rise slightly to 2.136 bil. bu. due to higher carry-in stocks from last year’s crop and lower usage, likely from feed/residual.

SOYBEANS

Prices were mixed as beans ranged from $.03 lower to $.01 higher, meal was $2-$3 lower while bean oil was up 50-55 points. Spreads weakened across the complex. Inside trade for Jan-26 beans as it holds close to its 16 month high. Dec-25 meal likely felt pressure from news Brazil is now approved to export both sorghum and DDG’s to China. Dec-25 oil shot up to a 3 week high drawing support from higher energy prices. Jan-26 crush margins improved $.02 ½ to $1.40 bu. while bean oil PV improved to a 2 week high at 44.6%. Mostly favorable weather conditions in Brazil should work to limit further upside potential. China has still not publicly acknowledged they have agreed to purchase 12 mmt of US beans by the end of the year, or 25 mmt every year over the next 3 MY’s. US FOB offers at the Gulf are already $.30 bu. over Brazilian offers for Jan. shipment and it only gets wider from there as we get deeper into Brazil’s harvest. This is even before the 10% tariff differential that works against the US competitiveness. China continues to show no interest in US soybeans. The average soybean production est. in the Reuters survey at 4.266 bil. bu. is down 35 mil. from Sept. and about 25 mil. above our estimate. Ending stocks however are expected to be little changed from the Sept forecast of 300 mil. bu. as the lower production is likely to be offset by lower demand, most likely exports due to the lack of sales to China. EU 25/26 soybean imports as of Nov. 9th at 4.15 mmt are down 16.5% YOY. Their meal imports at 6.5 mmt are down 4.3%.

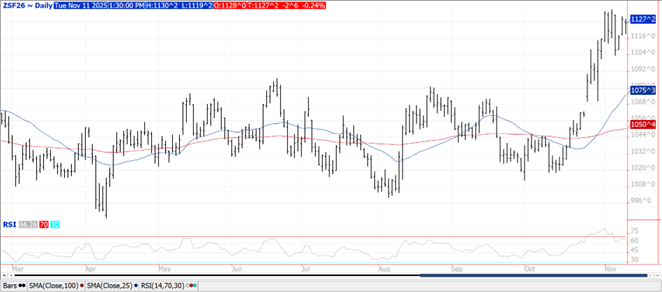

WHEAT

Prices range from $.03 lower in KC to $.05 higher in MIAX futures. Spreads weakened across all 3 classes. The Dec-25 contracts in both CGO and KC hover near their 100 day MA. Dec-25 MIAX futures traded to a 6 week high. Jordan reportedly bought 60k mt of wheat in their recent 120k mt tender paying 262.50/mt CF for Feb-26 shipment. EU 25/26 soft wheat exports as of Nov. 9th at 8.38 mmt are down 3.8% YOY. The Reuters survey shows the US wheat ending stocks are expected to rise about 25 mil. bu. to 867 due to the higher production forecast in the Sept. 30th USDA update just ahead of the shutdown.

Charts provided by QST.

Risk Warning: Investments in Equities, Contracts for Difference (CFDs) in any instrument, Futures, Options, Derivatives and Foreign Exchange can fluctuate in value. Investors should therefore be aware that they may not realise the initial amount invested and may incur additional liabilities. These investments may be subject to above average financial risk of loss. Investors should consider their financial circumstances, investment experience and if it is appropriate to invest. If necessary, seek independent financial advice.

ADM Investor Services International Limited, registered in England No. 2547805, is authorised and regulated by the Financial Conduct Authority [FRN 148474] and is a member of the London Stock Exchange. Registered office: 3rd Floor, The Minster Building, 21 Mincing Lane, London EC3R 7AG.

A subsidiary of Archer Daniels Midland Company.

© 2021 ADM Investor Services International Limited.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.