Written Commentary

SOYBEANS

Soybean market is back near 12.25 and what some feel is the midpoint of a range between 12.00-12.50

- 12.00 tends to trigger new demand. 12.50 may be high given favorable start to South America 2022

crops. Weekly US soybean exports were near 84 mil bu vs 64 last week and 86 last year. Season to date

exports are near 216 mil bu vs 437 last year. China has a lot of catching up to do. US soybean harvest is

est near 62 pct vs 49l;ast week. Cash basis is firming as harvest nears end. Brazil weather is favorable for

crops. Argentina is turning drier. SX range was 12.20-12.25. First resistance is near the 20 day moving

average and 12.50. USDA est US 2021 US soybean crop near 4,448 mil bu vs 4,216 last year. Crude is

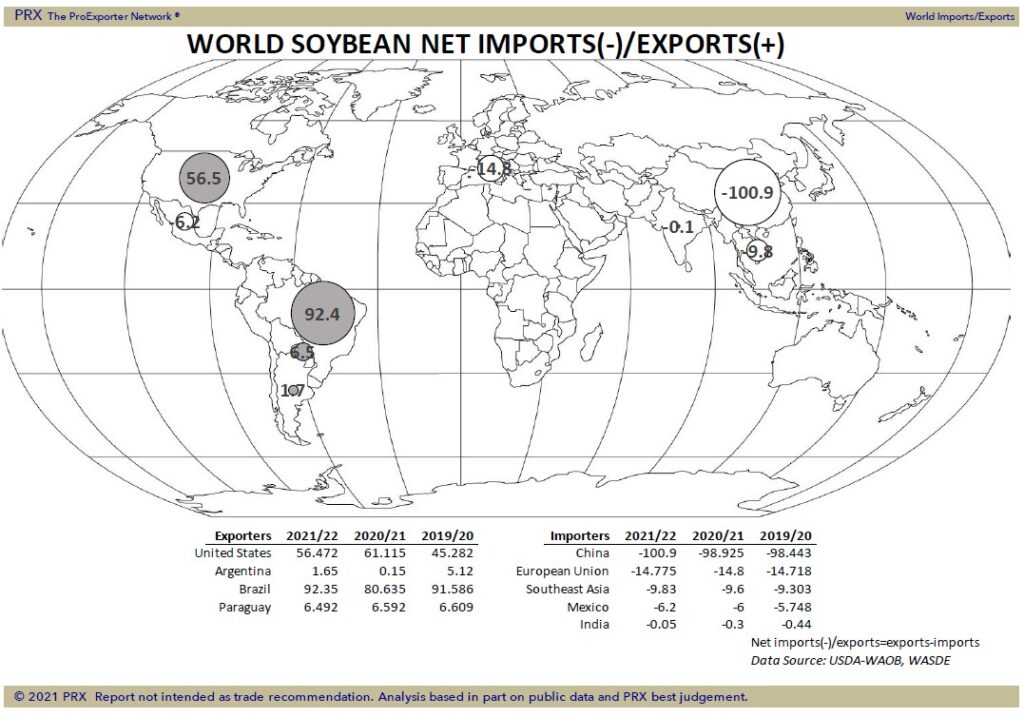

estimated near 2,190 vs 2,141 last year. Exports are estimated near 2,090 vs 2,265 last year. Some feel final exports could be 2,050. That could increase carryout 40 mil bu to 360. USDA increased crush due to higher US domestic soymeal use which added to the soyoil carryout. USDA also estimated World 2021/22 soybean end stocks near 104.5 mmt vs 99.1 ly. Brazil 2022 crop is est near 144 mmt vs 137 ly. Brazil soybean planting pace mis ahead of normal. USDA est Argentina 2022 crop near 51 mmt vs 46 ly.

CORN

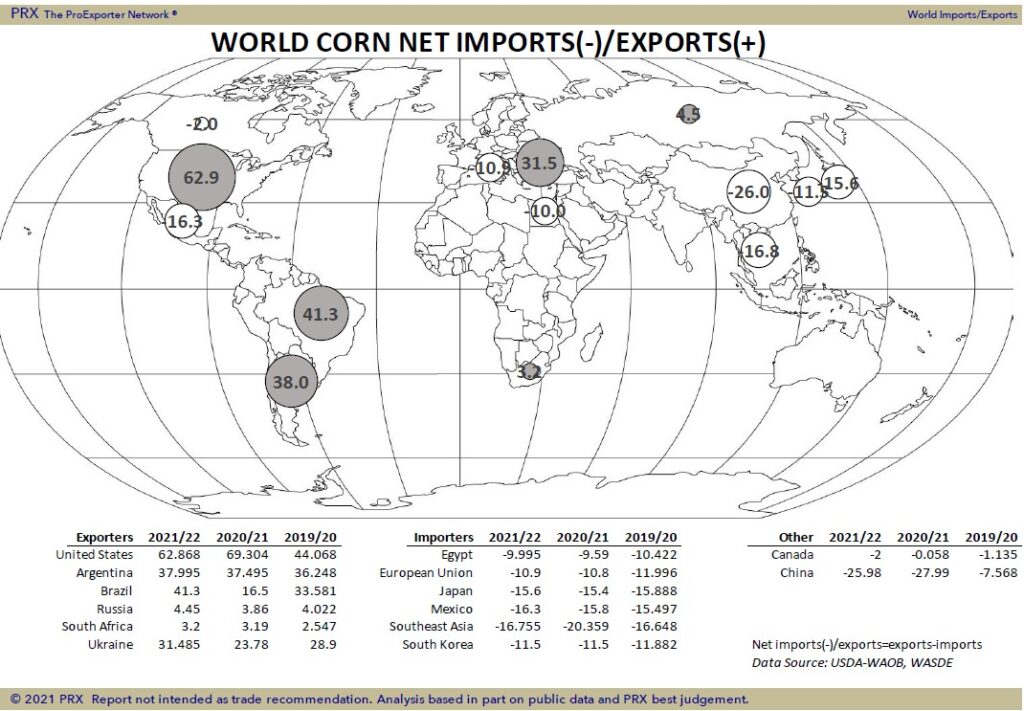

Corn futures closed higher and near session high. Corn futures started lower due to a drop in China Q3 GDP. China Q3 GDP was 4.9 pct vs 5.2 expected and Q2 7.9. Corn market is back near 5.33 and what some feel is near the high of a range between 5.10-5.40 CZ. 5.10 tends to trigger new demand. 5.40 may be high given favorable start to South America 2022 crops. Weekly US corn exports were near 38 mil bu vs 36 last year. Season to date exports are near 161 mil bu vs 216 last year. Cash basis is firming on increase end user buying. CZ range was5.23-5.33. Next resistance is near 5.35 then 5.40 the 5.47. USDA est US 2021 US corn crop near 15,019 mil bu vs 14,111 last year. Feed is estimated near 5,650 vs 5,597 last year. Exports are estimated near 2,500 vs 2,753 last year. Some feel final exports could be 2,700. Ethanol is 5,200 vs 5,032 ly. That could lower carryout 200 mil bu to 1,300. USDA also estimated World 2021/22 corn end stocks near 301.7 mmt vs 290.0 ly. Brazil 2022 crop is est near 118 mmt vs 86 ly. Early corn planting was delayed which could add to 2nd crop acres. USDA est Argentina 2022 crop near 53 mmt vs 50 ly. La Nina could dry Argentina crop areas.

WHEAT

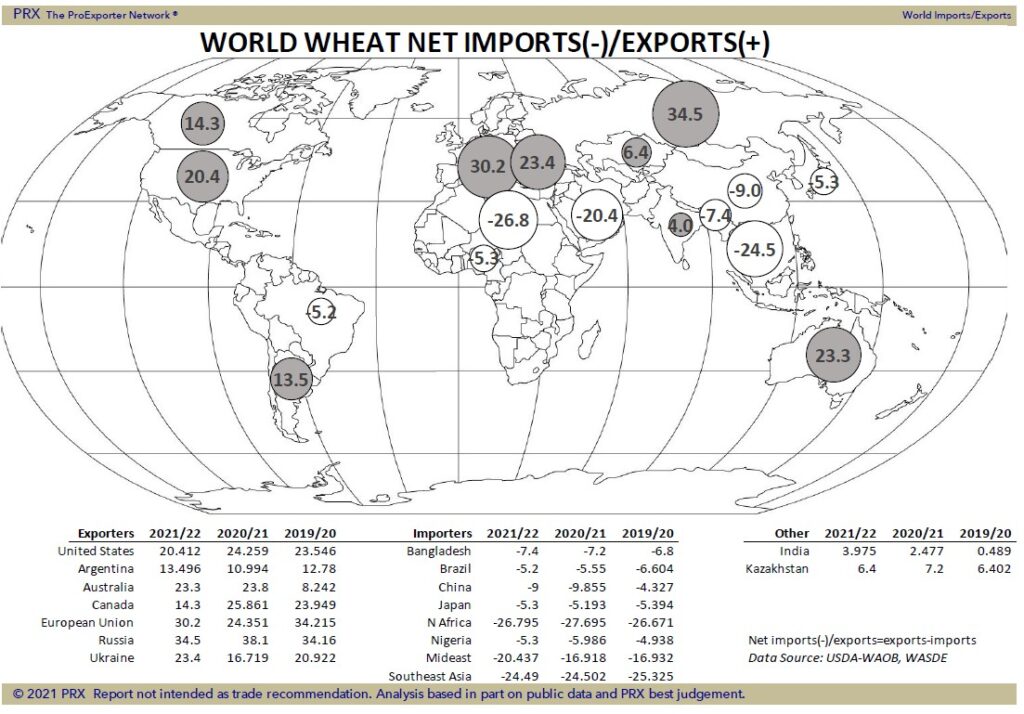

Wheat futures closed mixed. Chicago and KC closed higher. Minn was slightly lower. The N Africa and Middle East buyers are short. World milling wheat stocks are record low. US World exporters stocks to use ratio is also record low. There is talk that EU wheat exports will slow and after Jan 1 Russia exports could slow. Concern about inflations and slower US/World food demand could lower demand. Wheat market is near 7.35 and what some feel is near the midpoint of a range between 7.00-7.70 WZ. 7.00 tends to trigger new demand. 7.70 may be high given favorable USDA outlook for World 2022 crops. Weekly US wheat exports were near 5 mil bu vs 9 last year. Season to date exports are near 343 mil bu vs 392 last year. After Jan 1, US HRW export prices are competitive to buyers. La Nina could reduce rains in 2022 across US HRW crop area. USDA Est World 2021/22 wheat crop near 776 mmt vs 774 last year. EU 139 vs 126 ly. Russia 72.5 vs 85, Canada 21 vs 35 ly, Austrália 31,5 vs 33 and Ukraine 33 vs 25 ly, US

Risk Warning: Investments in Equities, Contracts for Difference (CFDs) in any instrument, Futures, Options, Derivatives and Foreign Exchange can fluctuate in value. Investors should therefore be aware that they may not realise the initial amount invested and may incur additional liabilities. These investments may be subject to above average financial risk of loss. Investors should consider their financial circumstances, investment experience and if it is appropriate to invest. If necessary, seek independent financial advice.

ADM Investor Services International Limited, registered in England No. 2547805, is authorised and regulated by the Financial Conduct Authority [FRN 148474] and is a member of the London Stock Exchange. Registered office: 3rd Floor, The Minster Building, 21 Mincing Lane, London EC3R 7AG.

A subsidiary of Archer Daniels Midland Company.

© 2021 ADM Investor Services International Limited.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.