Written Commentary

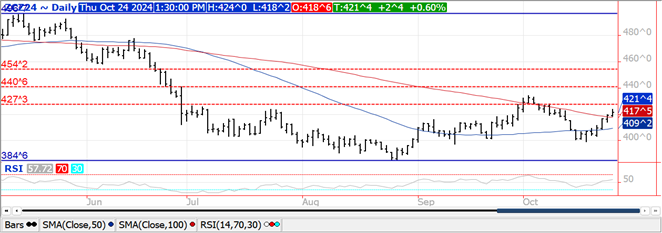

CORN

Prices were up $.02-$.03 in choppy 2 sided trade. While the Dec-24/Mch-25 spread weakened a touch, deferred spreads firmed up. Dec-24 traded to a fresh 2 week high before backing up. The 100 day MA now serves as support at $4.17 ½. The next major resistance is not until the Oct-24 high at $4.34 ¼. Outside of a few passing showers across the central Midwest over the next 24-36 hours US harvest weather remains favorable into month-end. Much above normal temperatures are expected to extend into early November however much needed precipitation is expected in week 2 of the outlook for much of the nation’s midsection. Export sales at 165 mil. bu. (142 mil. – 24/25 MY, 23 mil. – 25/26) were above expectations. The 24/25 sales were the highest weekly sales in 3 ½ years and bring YTD commitments to 924 mil. bu. up 34% from YA, vs. the USDA forecast of up 1%. Current commitments represent 40% of the USDA forecast, above the historical average of 38%. Noted buyers last week were Mexico – 66 mil. old crop and 23 mil. bu. new crop, unknown – 46 mil., and Japan – 10 mil. In addition the USDA announced fresh sales of 228k mt (9 mil. bu.) of corn to Japan and another 165k mt (6.5 mil.) to an unknown buyer. The current USDA export forecast at 2.325 is likely to be raised again in the Nov-24 WASDE. US corn area in drought increased 14% LW to 76%, the highest in the past year and triple where it was only 4 weeks ago.

SOYBEANS

Prices were mixed with beans closing within $.01 ½, of unchanged, meal was down $2-$5 while bean oil was up 80-95. After trading into only $.02 ¾, a 15 month high, the Nov-24/Jan-25 spread collapsed closing back out to $.08 3/4. Meal spreads also weakened while oil spreads were slightly firmer. Nov-24 beans failed to hold trade above the $10 level and its 50 day MA resistance. Next support is LW’s low at $9.68 ¼. Dec-24 meal closed near session lows however held support above its Oct. low at $308.80. Dec-24 oil peaked just below its Oct-24 high at 45.29. Spot board crush margins improved $.01 ½ to $1.74 ¼ bu. while bean oil PV improve to 41.7%, nearly a 7 month high. Malaysian palm oil prices reached a fresh 2 year high while also extending its premium over spot soybean oil futures. South American weather remains favorable as a good mix of rain and sunshine the next few weeks in Brazil will keep the outlook for planting progress and crop development favorable. In Argentina, recent heavy rains across key growing areas in the central part of the country were deemed a “game changer” by the Rosario Grain Exchange in helping improve corn and wheat crop prospects. Export sales at 79 mil. bu. were a new MY high however in line with expectations. YTD commitments have reached 882 mil. up 8% from YA vs. the USDA forecast of up 9%. Commitments represent 48% of the USDA forecast, below the historical average of 56%. China/unknown combined to purchase 52 mil. bu. bringing combined commitments to 585 mil. bu. below the 594 mil. from YA and well below the 906 mil. from 2022. In addition the USDA announced the sale of 198k mt (7 mil. bu.) to an unknown buyer. Soybean meal sales at 160k tons were at the low end of expectations. YTD commitments are down 3% from YA, vs. the USDA forecast of up 9%. Soybean oil sales at 29k tons were in line with expectations. Soybean areas in drought also increased 14% to 68%, a 52 week high.

WHEAT

Prices recovered to close $.01-$.03 higher across all 3 classes. The recovery effort in Chicago Dec-24 stalled right at its 100 day MA at $5.84 ¼. One way or another Dec-24 KC wheat will break out above its 100 day MA resistance or below its 50 day MA support. Southern and western Australia remain in a dryer than normal pattern further stressing small grain production. Export sales at 20 mil. bu. in line with expectations and bring YTD commitments to 481 mil. up 18% from YA, vs. the USDA forecast of up 17%. YTD by class sales are: HRW +46% vs. USDA +64%, SRW -17% vs. -27%, HRS +14% vs. +13% and white +44% vs. +28%. The USDA Ag. Attaché to Australia forecasts their 24/25 wheat production at 28.5 mmt, well below the official USDA forecast of 32 mmt. They’re also estimating exports at only 20 mmt, 5 mmt below the USDA forecast from earlier in October. Despite over 2 ½ years of war, Ukrainian grain exports since July 1st for the 24/25 MY have reached 13.3 mmt, vs. only 8.3 mmt YA. Wheat shipments have reached 7.3 mmt, up 77% while corn shipments at nearly 4 mmt are up 17%.

All charts provided by QST.

>>See more market commentary here.

Risk Warning: Investments in Equities, Contracts for Difference (CFDs) in any instrument, Futures, Options, Derivatives and Foreign Exchange can fluctuate in value. Investors should therefore be aware that they may not realise the initial amount invested and may incur additional liabilities. These investments may be subject to above average financial risk of loss. Investors should consider their financial circumstances, investment experience and if it is appropriate to invest. If necessary, seek independent financial advice.

ADM Investor Services International Limited, registered in England No. 2547805, is authorised and regulated by the Financial Conduct Authority [FRN 148474] and is a member of the London Stock Exchange. Registered office: 3rd Floor, The Minster Building, 21 Mincing Lane, London EC3R 7AG.

A subsidiary of Archer Daniels Midland Company.

© 2021 ADM Investor Services International Limited.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.