Written Commentary

SOYBEANS

Soybeans, soymeal and soyoil traded higher. Market might be trying to liquidate short positions before long holiday weekend and before next weeks USDA Sep crop report. Fact this weeks US soybean and Soymeal export sales were higher than expected may have also offered support. Finally, this weeks selloff in prices was linked mostly to damage to US gulf export infrastructure due to the Hurricane and some hope next week some of the elevators get power restored. For the week. SX ranged from a high near 13.36 to a low near 12.70. SX ended near 12.92. Some are beginning to buy SX and sell SX2 looking for SX to be supported by increase China buying. Informa est US soybean yield near 50.0.

CORN

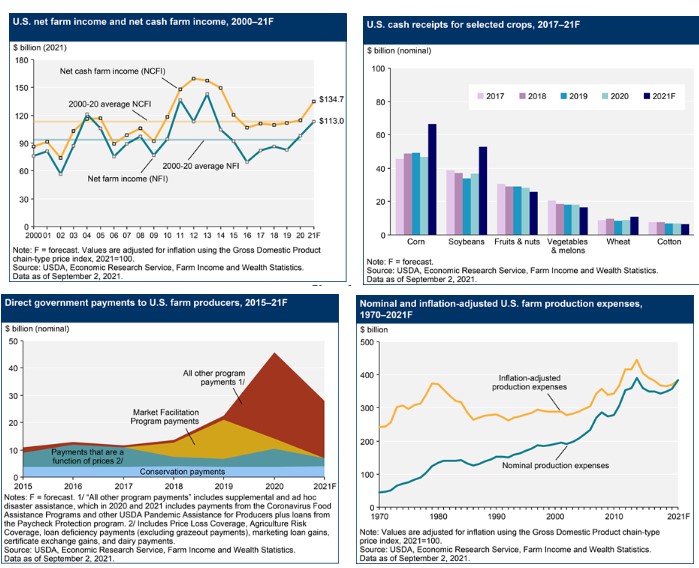

Corn futures ended slightly lower. Managed funds continue to liquidate net longs going into US harvest and USDA Sep crop report. This weeks US corn export sales were higher than expected. This and lack of farmer selling offered support. Some feel CZ will continue to lose to CH2 through harvest. Funds may be more willing to buy corn post US harvest and once China begins to buy US corn. This week CZ dropped from a high near 5.58 to a low near 5.15 after Hurricane damaged US gulf export infrastructure. Market prices could rebound once power is reported to US gulf elevators. Informa est US 2021corn yield near 175.4 vs USDA 174.6, US sorghum yield to 73.1 vs USDA 70.8. Informa lowered EU corn crop 1.4 mmt to 64.1. Along with new 2021 corn yields on their Sep 10 report, NASS will also resurvey US corn, sorghum, oats and barley acres. Most look for higher 20/21 corn carryout and lower 21/22 corn carryout. Lower US 21/22 corn carryout due to higher export demand. USDA estimated US 2021 farmer net income up 19 pct to $113 billion. In Feb, they est income to drop 8 pct due to lower government payments and higher cost. 2021 farm expenses were up 7 pct to $383 billion.

WHEAT

For most of the week, wheat futures traded lower and followed lower trade in corn and soybeans. Lower corn and soybean trade linked to hurricane damaging US gulf export infrastructure. US weekly export sales were near trade estimates but remain behind last years pace. Talk of lower Canada and Russia crops and export supplies could help wheat futures. This week there was additional talk that the Russian wheat crop could be down enough to substantially lower their exports. Informa est US all Wheat crop near 1,628 mil bu vs USDA 1,697. HRW was est at 785 vs USDA 777, SRW 362 vs 366, HRS 239 vs 305 white 211 vs 214 and durum 31 vs 35. Informa lowered Canada wheat crop 1.0 mmt to 23.0, EU wheat crop 2.8 to 135.8 and Kazakhstan crop 1.5 to 11.0. WZ ended near 7.26 with weekly range 7.43 to 7.05.

Risk Warning: Investments in Equities, Contracts for Difference (CFDs) in any instrument, Futures, Options, Derivatives and Foreign Exchange can fluctuate in value. Investors should therefore be aware that they may not realise the initial amount invested and may incur additional liabilities. These investments may be subject to above average financial risk of loss. Investors should consider their financial circumstances, investment experience and if it is appropriate to invest. If necessary, seek independent financial advice.

ADM Investor Services International Limited, registered in England No. 2547805, is authorised and regulated by the Financial Conduct Authority [FRN 148474] and is a member of the London Stock Exchange. Registered office: 3rd Floor, The Minster Building, 21 Mincing Lane, London EC3R 7AG.

A subsidiary of Archer Daniels Midland Company.

© 2021 ADM Investor Services International Limited.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.