China will begin charging a 34% tariff on all US imports this Thursday, April 10th. Details of their response against the new US trade policies are still being deliberated. So far, Beijing authorities have announced restrictions on exporting 7 different earth metals, a halt of chicken products from two US companies, they added export controls on 16 US companies, stopped all sorghum imports from the US, they are now investigating DuPont China or antitrust violations, and they added 11 US defense companies to an unreliable entity list.

AG FUNDAMENTALS:

This Thursday, April 10th, the USDA will release their monthly WASDE report. The 2025/2026 new crop numbers will not be out on this week’s report but rather on the May 12th report. Expectations are a readjustment to the demand side of the balance sheet. Corn exports and ethanol demand has been higher than the pace needed to reach the current estimates. So bulls are hope to see an increase of 25-50 million bushel between those two demand outlets, but corn feed and residual may under perform expectations by -50M to over -100M bushels. We will see planting progress per state released later this afternoon. Rains in the southern regions will put many farmers in KY, southern MO, TN, AR and northern MS slightly behind pace for now. Soybeans have felt the most pain with an over 50¢ drop year to date. The mixture of increased tensions with our largest soybean trade partner, China, and the cooperative weather in South America has allowed their soybean harvest to progress on schedule. Funds and Managed Money were both friendly soybeans and soybean oil last week, but most speculators have set up camp on the sidelines until more information is reveled. Any day now there could be an announcement, foreign or domestic regarding trade policies as negotiations over tariffs continue. Wheat is leading the charge back this morning as weather in the US and pending crop conditions are giving life to the wheat complex. Today’s state-by-state crop condition report should help shed more light on the current state of the US winter wheat crop.

The S&P 500 Weekly Chart shows we have hit the 50% retracement of the October 2022 low to the recent all-time high.

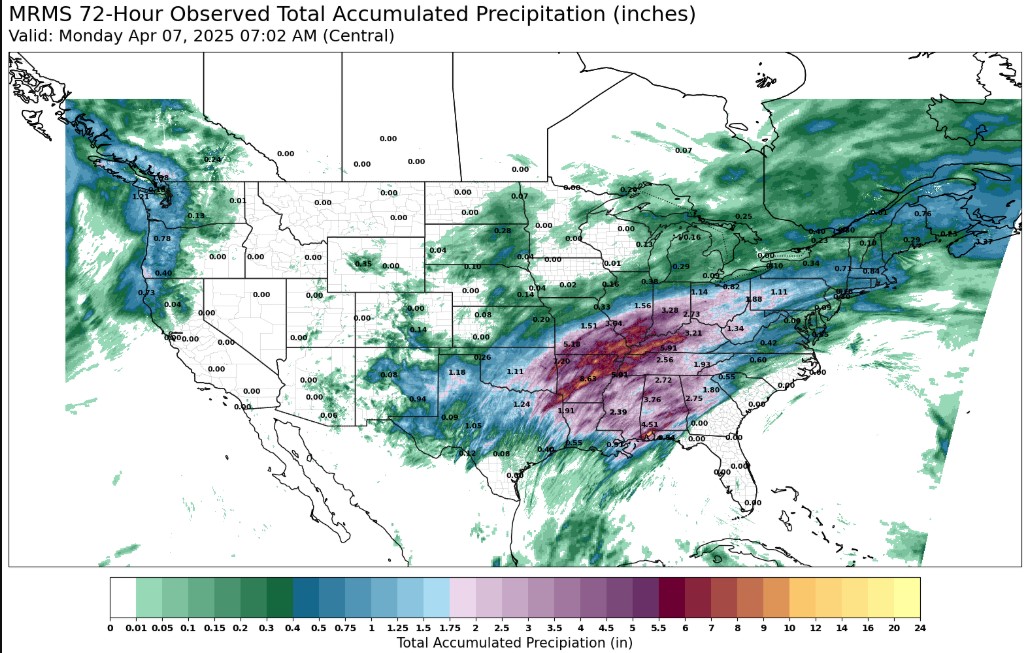

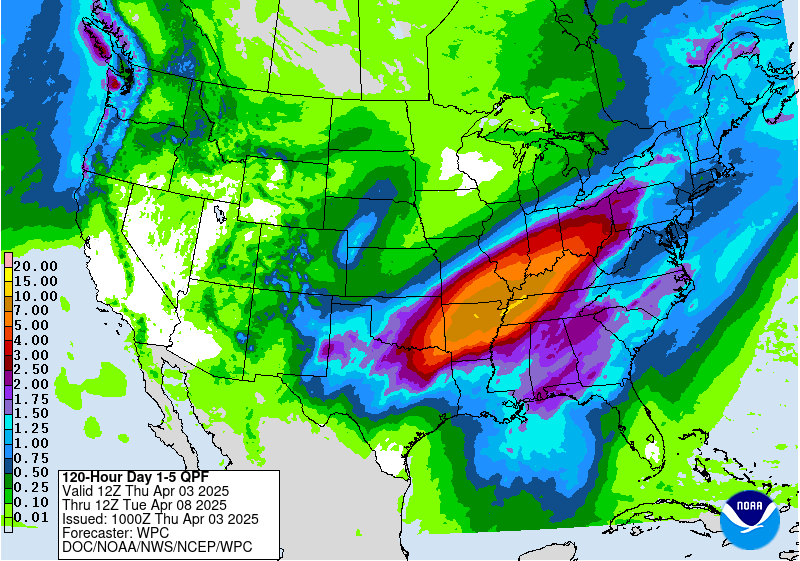

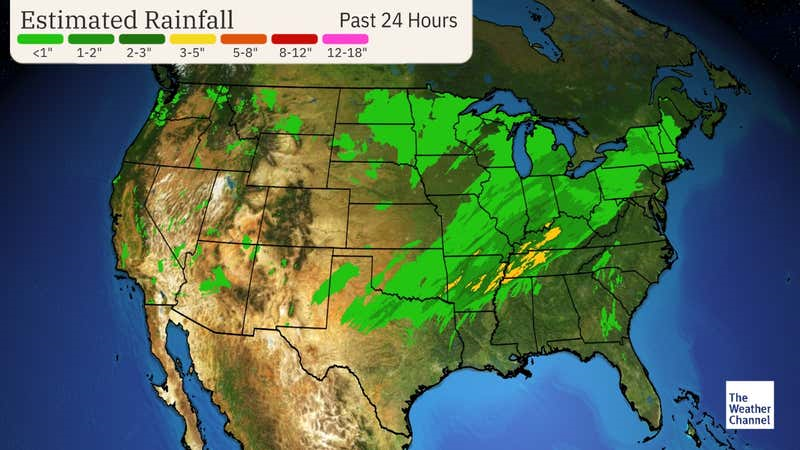

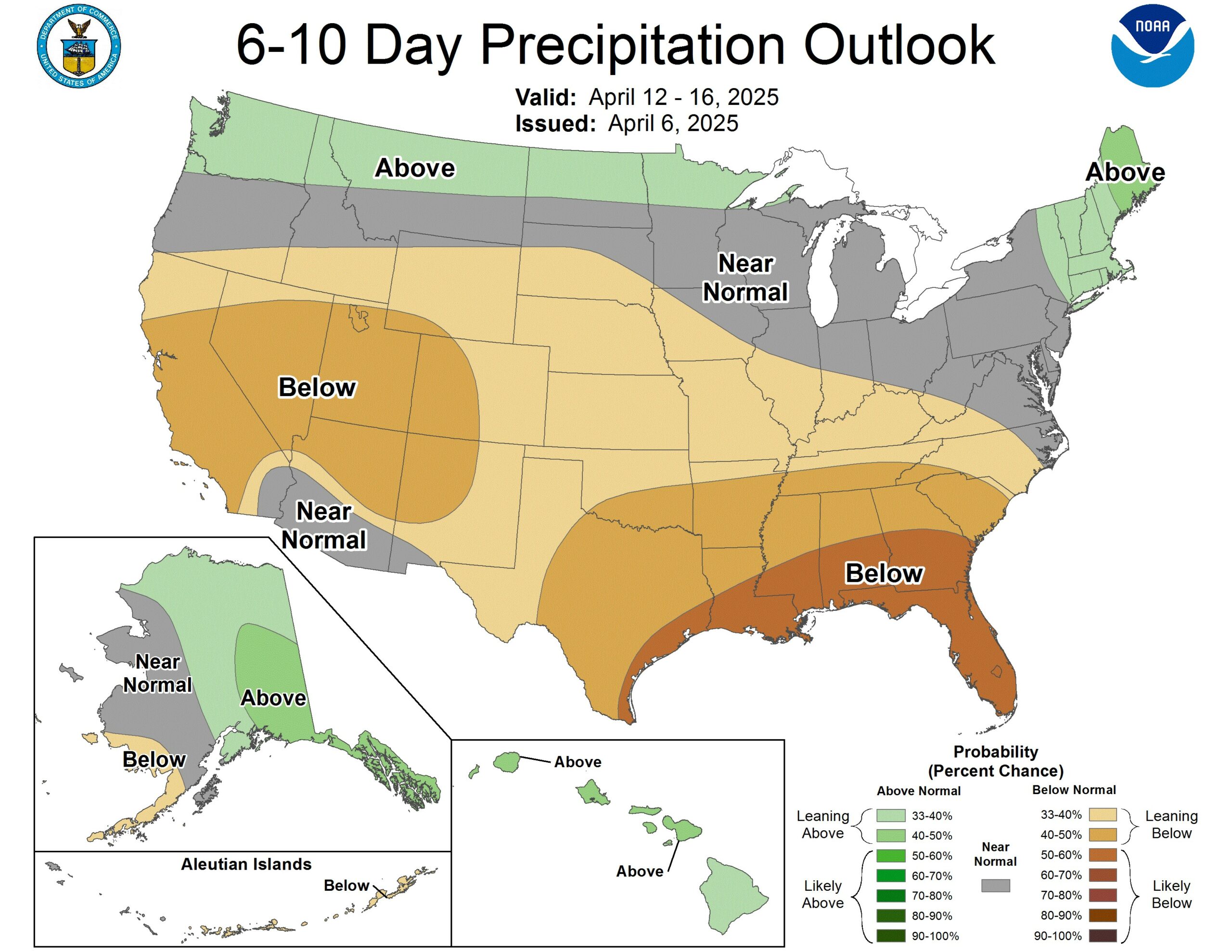

The Last 72 Hours of Rainfall shows heavy rains in the south and southern Midwest will slow down planting progress for days until fields dry out. Parts of eastern KY received up to a foot of rain in the last 5 days.

Export & World News

Algeria issued an international tender to purchase 50K MT of durum wheat from optional origins.

Malaysian palm oil futures were down 146 ringgit overnight, at 4182.

>>Interested in more commentary by Joe Mauck? Go HERE

Risk Warning: Investments in Equities, Contracts for Difference (CFDs) in any instrument, Futures, Options, Derivatives and Foreign Exchange can fluctuate in value. Investors should therefore be aware that they may not realise the initial amount invested and may incur additional liabilities. These investments may be subject to above average financial risk of loss. Investors should consider their financial circumstances, investment experience and if it is appropriate to invest. If necessary, seek independent financial advice.

ADM Investor Services International Limited, registered in England No. 2547805, is authorised and regulated by the Financial Conduct Authority [FRN 148474] and is a member of the London Stock Exchange. Registered office: 3rd Floor, The Minster Building, 21 Mincing Lane, London EC3R 7AG.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.