Written Commentary

A busy day for statistics to end the week with Japan’s National CPI, UK GfK Consumer Confidence and Retail Sales along with South Korea’s April 1-20 Exports to digest, but the focus will be on G7 flash PMIs, which are accompanied by Canadian Retail Sales. There is a smattering of Fed and ECB speakers, and the hardly diplomatic comments from BoE’s soon departing Tenreyro likening hawkish members of the MPC to Milton Friedman’s “fool in the shower”. Italy will sell 2-yr and inflation-linked 5-yr. On the earnings front, Great Wall Motor and SAP will be among the headline makers, while the US eyes Freeport-McMoRan, HCA Healthcare, Procter & Gamble and Schlumberger, though the dramas around Tesla, SpaceX and Twitter over the past 48 hours may be the bigger discussion point for markets’ chattering classes.

Next week’s schedule has a lot of major data, including advance Q1 GDP readings for the US, South Korea and many EU countries, which also have provisional April CPI readings for April, as well as a raft of surveys including Germany’s Ifo and GfK. The US will also look to Personal Income/PCE, Durable Goods Orders, Consumer Confidence, House Prices, Goods Trade Balance, Pending Home Sales and more regional Fed surveys. While Japan has its usual end of month Tokyo CPI, Industrial Production and Retail Sales, all eyes will be on the BoJ policy meeting which concludes on Friday. New governor Ueda has been at pains to signal that there will be no change in policy at that meeting, but markets remain understandably very wary about any signals on a potential future shift from its ultra-accommodative policy stance, even more so after the March ‘core core’ CPI was higher than expected at 3.8%, and at its highest y/y level since 1981.

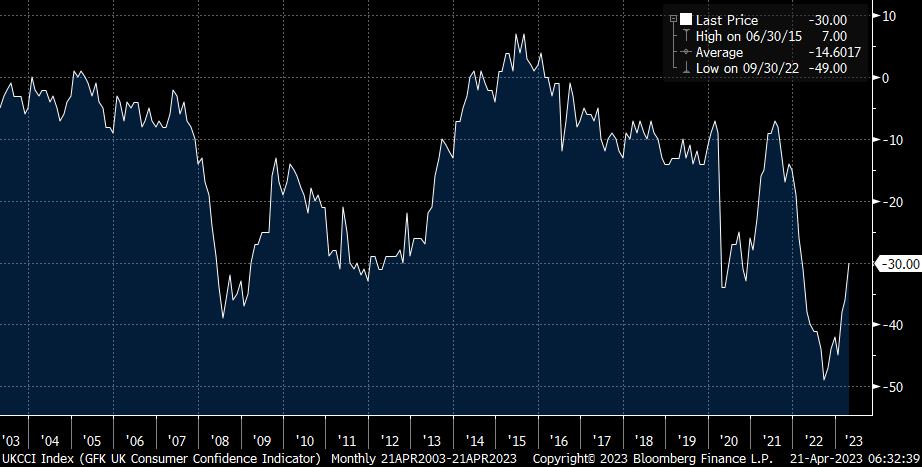

** U.K. – April GfK Consumer Confidence & March Retail Sales **

GfK Consumer Confidence continued its relatively sharp recovery, with a third consecutive rise to -30 from -36, paced both by improving views about Personal Finances and the Economic Situation, and somewhat less by the Climate for Major Purchases (-28 vs. -33). But as the attached chart highlights, it is still only modestly above pandemic and GFC lows, though the trend is clearly one of solid improvement. Retail Sales were a little weaker than expected falling 0.9% m/m -3.1% y/y, and effectively correcting the exaggerated strength of January and February, but nevertheless still expanding overall in Q1.

** G7 – April ‘flash’ PMIs **

G7 PMIs are expected to confirm established trends for manufacturing (contracting) and Services (expanding at a healthy if not robust pace), with UK and Eurozone Manufacturing improving fractionally, while the US is seen easing marginally; and Services easing relative to February across the board, but more sharply in the US. There will inevitably be one or more surprises, but it will be the details on Orders and Output, and Services’ New Business which should attract most attention.