Written Commentary

With the Iran/USA ceasefire extended, but no signals on when negotiations might resume, markets are likely to trade cautiously, with a rather limited run of economic data, featuring UK CP, Japan Trade and Eurozone Consumer Confidence (set to dive if the slide in the Dutch Consumer Confidence measure to -44 from -30 is any guide), the Bundesbank’s monthly report and a flurry of ECB speakers and a busier run of US corporate earnings (Boeing, Tesla and Texas Instruments among the highlights) offering some distractions.

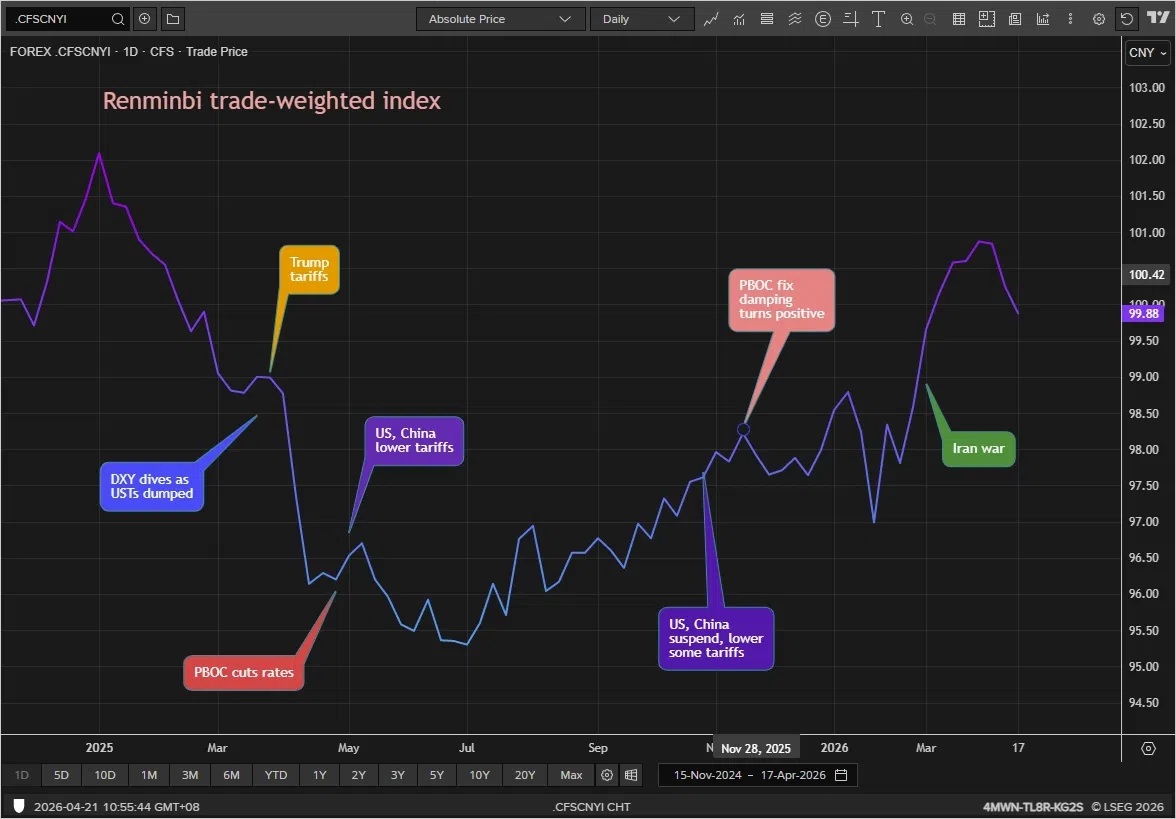

While the military confrontation may be on hold, the risks from the disruptions to supply chains continues to grow, and by extension skews the risk of longer-term adverse inflationary pressures ever higher. In that regard, it is worth noting that while the seemingly relentless rise of the CNY has been checked by the Middle East War (see CNY Trade Weighted Index chart), the PBoC and local authorities probably view a stronger Yuan limiting the impact of higher energy and commodity prices, per se improving domestic purchasing power and partially offsetting the impact of higher resource prices on already domestic demand. Indirectly, a stronger CNY also helps to rein in its large trade surplus, though that impact is likely to be rather more marginal, and the authorities will be more wary of a very real potential threat from higher energy prices to export demand above all from Asia and Europe.

** U.K. – March CPI **

While Transport (i.e. road fuel prices) was unsurprisingly the biggest contributor along with airfares to the marginally higher than expected 0.7% m/m 3.3% y/y increase in CPI, there was also some renewed upward pressure on Food, as well as from Restaurants & Hotels. That in turn accounted for divergence in the small dip in core CPI to 3.2% as against higher than expected Services CPI at 4.5% (vs. forecast 4.3%), which will likely prompt some of the MPC hawks to vote for a rate hike in May. The larger than expected 4.4% m/m surge in PPI Input was largely energy related, though core PPI Input was up a more modest 0.6% m/m, and unchanged in y/y terms at 1.7%, while PPI Output showed only limited signs of ‘pass through’ effects at 0.9% m/m, but the litmus test on this will come with Q2 readings. As with the ECB, the MPC majority is still likely to be cautious about raising rates precipitously.