Written Commentary

A heavily front-loaded data schedule has UK CPI, Japan’s Orders and Trade to digest, with South Africa CPI and US Existing Home Sales, while the FOMC minutes and much anticipated earnings from AI tech darling Nvidia top the events schedule. There are also the as expected no change RBNZ (though very hawkish) and Bank Indonesia rate decisions to digest, and a further run of central bank speakers; other corporate earnings to garner some attention will likely include: British Land, Marks & Spencer, Severn Trent, Analog Devices and Target. A busier day for govt bond auctions has UK 5-yr, German and Canadian 10-yr, and US 20-yr, following rather tepid demand for Japan’s 40-yr sale, which also saw 10-yr JGB yields hit 1.0% for the first time in 11 years.

** U.K. – April CPI & PPI **

– Sharp rises in Health and Restaurants & Hotels (both 0.9% m/m), Miscellaneous Goods & Services (0.8% m/m) offset some of the downward pull from the lowering of the household energy price cap, with Transport (1.7% m/m) and Communication (4.5% m/m) also posting large monthly gains, though still less than in April 2023. While headline CPI at 2.3% y/y is close to the BoE’s target, core CPI at 3.9% y/y and above all the marginal fall in Services CPI (5.9% y/y vs. prior 6.0%) will have the majority of the MPC pushing back on their rate cut timelines. The latest Brightmine (formerly XpertHR) wage settlements data (4.9% y/y vs. 4.6%) most likely reflects an upward pull from the April rise in the National Living Wage, but will also serve to keep Services prices elevated. While the May CPI data will be published before the next MPC meeting, it would need to see a seemingly unlikely and much sharper drop in Services prices to prompt an initial rate cut in June.

** U.S.A. – FOMC minutes **

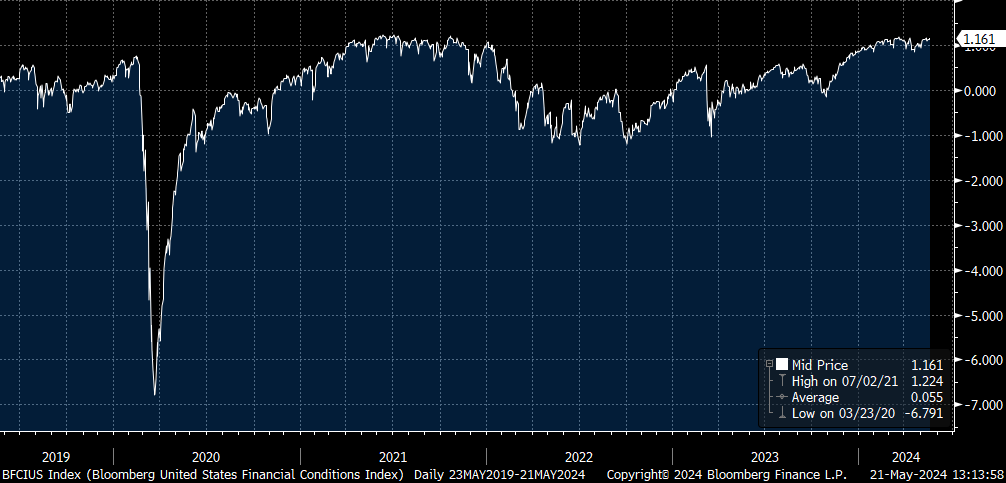

– The message from Powell’s press conference and statement was that a further rate hike is not on the table (and a discussion about the ‘neutral rate’ deemed to be rather moot), but inflation still needs to turn lower again, and growth to moderate and the labour market to loosen to put a rate cut on the table. Eminently the likes of Bowman and Mester have reiterated they would hike rates again if needed, but in truth the bar to a further hike is high, and as the RBA noted yesterday runs the risk of unnecessary micro-management that undermines any central bank’s credibility. It will be interesting to see if the discussion on inflation, growth and the economy echoes Waller yesterday: “In the absence of a significant weakening in the labor market, I need to see several more months of good inflation data before I would be comfortable supporting an easing in the stance of monetary policy”; and indeed if there was any concern about loose US financial conditions, which has become more acute since the last FOMC meeting.