Written Commentary

While the statistical run has rather more meat on the bone today, it is likely to be subordinate to the run of US Q1 earnings, which features a broad sectoral array of major US corporates. There are South Korean Q1 GDP (as expected) and UK PSNB budget data (marginally better than forecast) to digest, with the CBI Industrial Trends survey ahead (quite possibly the last of any significance, given the scandal engulfing organization probably did not affect the number of responses this month). The US looks to Consumer Confidence, FHFA and CoreLogic CS House Prices, New Home Sales, and Richmond and Dallas Fed surveys. BoE’s Broadbent and ECB’s de Cos are the day’s central bank speakers, with Hungary’s MNB seen holding rates at 13.0%, while South Africa’s SARB publishes its biannual Monetary Policy Review. Alphabet and Microsoft offer the first of this week’s US ‘Megatech’ earnings reports, while other likely headline makers include: 3M, ADM, Dow, General Motors, Halliburton, McDonald’s, PepsiCo, PulteGroup, Raytheon, Texas Instruments, UPS, Verizon and Visa. Govt bond supply takes the form of 2-yr auctions in Germany and the USA.

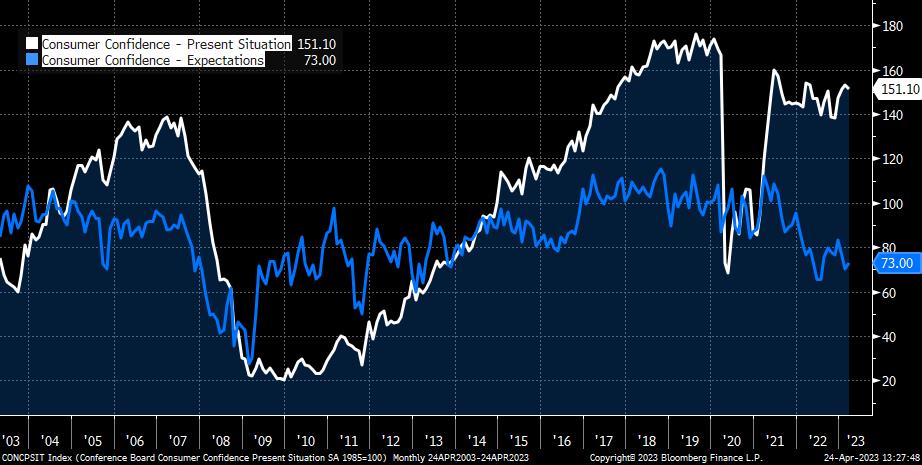

** U.S.A. – Apr Consumer Confidence,, Mar New Home Sales & Feb House Prices **

– Consumer Confidence is seen little changed at 104.0 (vs. March 104.2), some loosening in labour market conditions suggests some downside risks, on the other hand the flash PMIs (above all Services) showed some resilience. What remains very notable is that Expectations remain very depressed (even lower than the Pandemic low), despite the continued buoyancy of the Present Situation Index, and a still very robust Labour Market differential (jobs ‘plentiful’ minus ‘hard to get’). Both FHFA and CoreLogic House Prices are expected to drop again in m/m terms, which would take the CoreLogic measure just into negative territory at -0.1% y/y. New Home Sales are seen dropping 1.6% m/m after 3 months of solid gains, with higher mortgage rates and persistent affordability challenges continuing to present considerable headwinds, even if the slide in the housing market does look as though it is bottoming out.