Written Commentary

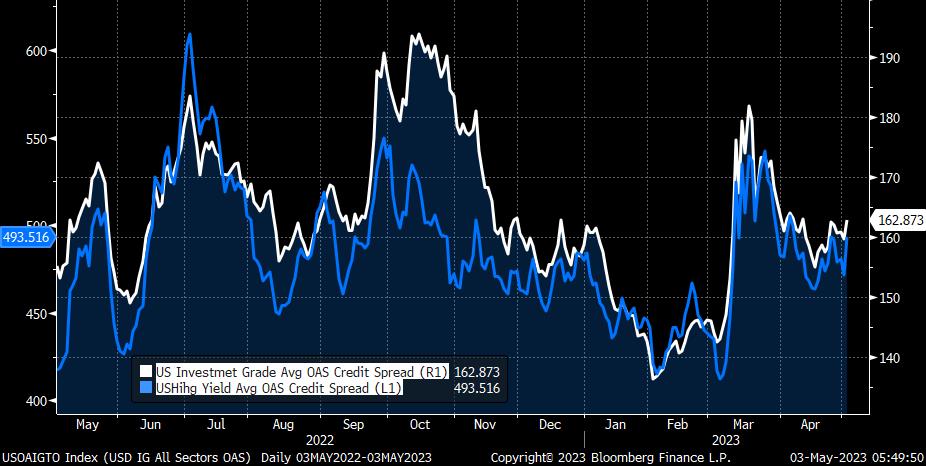

The FOMC meeting dominates the day’s proceedings, with a modest run of economic data featuring Australian Retail Sales, Turkish CPI and US ADP Employment and Services ISM/PMI. As expected Malaysia’s BNM held rates at 2.75%, while both Czechia’s and Brazil’s BCB are seen holding rates at 7.0% and 13.75% respectively. The US corporate earnings schedule is likely to see Albemarle, Bunge, Marathon Oil, Metlife, Mosaic, Phillips 66, Qualcomm and Zillow among the headline makers. Govt bond auctions take the shape of 2-yr and German 5-yr. As can be seen in the attached chart on credit spreads, credit markets have again been jolted out of another bout of goldilocks thinking by the seizure and sale of First Republic Bank.

While concerns about the global, and above all China economic outlook are weighing heavily on oil prices, the outsized fall yesterday is as much testament to lack of market depth and participation with volumes having slid to levels normally associated with year-end, as can be seen on the attached chart.

As with the short squeeze in Sofr futures, this will only add to the risk of large volatility and price spikes (up/down), and with margin call financing becoming an ever larger problem, the risk of dislocations in markets and smaller and medium size trading companies become ever higher.

** U.S.A. – FOMC rate decision **

The consensus looks for a 25 bps hike to a 5.0-5.25% Fed Funds target, and outside of Chicago Fed’s Goolsbee, there would appear to be a strong FOMC consensus backing this move. The labour market remains relatively tight; the US GDP report saw Final Sales to Domestic Buyers at a robust 3.2% SAAR, even if Private Consumption at 3.7% was flattered by seasonal adjustment, and the March core PCE deflator at 4.6% y/y just how sticky core inflation remains, and how slowly it is coming down, and the Employment Cost Index at 1.1% q/q showed that wage pressures while not accelerating, are also not moderating. Eminently the FOMC will also have the latest Senior Loan Officers’ survey (covering the period up until early April) to hand, which will capture the extent of the tightening of credit conditions since the collapse of SVB and Signature Bank, and the initial but ultimately failed attempt to shore up First Republic Bank, which will weigh heavily in the FOMC’s deliberations, and the extent to which it is cited at this meeting (it should be published next week) will be of interest. The consensus also looks for the statement to signal a pause on rate hikes, by dropping ‘some additional policy firming may be appropriate’, and replace it with something that acknowledges that rates are ‘sufficiently restrictive’ to justify a pause, but emphasize that the FOMC stands ready to raise rates again if inflation does not come down as they anticipate, a point which will Powell likely double down on during the press conference, and markets should be wary of following yesterday’s RBA rate hike.

** U.S.A. – April ADP Employment, Services ISM **

The ADP Employment measure is seen little changed at 148K vs. March’s 145K, suggesting labour demand has been very steady since the start of the year, though clearly running at a slower pace than Q4; but as is well documented the ADP survey is a poor predictor of Payrolls, but remains a useful guide to the details of the Household survey. As with a modest drop in the ‘quit rate’ in yesterday’s JOLTS report, and indeed comments on the labour market in the Beige Book for today’s meeting, labour demand has cooled, but thus far shows minimal impact from the cumulative Fed rate hikes. As for the Services ISM, a modest uptick to 51.8 from March’s 51.2 is expected, with the anecdotal evidence from the PMI and regional Fed services surveys painting a dissonant picture, given the former posted a 12-month high at 53.7, while the NY survey flatlined and the Philly Fed measures slid sharply. In the details Prices Paid will require particular attention having fallen to 59.5 in March, its lowest level since September 2020, which in the medium term should translate into some downward pressure on the core Services PCE deflator. One general point that needs to be observed is that with manufacturers and services companies struggle to deal with very unpredictable demand trends in the aftermath of Covid and the Russian invasion of Ukraine, greater volatility in PMIs should be an assumption, along with a higher risk of inventory shocks (both too high and too low), and per se second derivative analyses of monthly data will be rather more tenuous.