Written Commentary

Today’s schedule of data has some significant items, via way of the overnight China CPI & PPI, weak Swedish monthly GDP, higher than expected Norwegian CPI, with Italian Industrial Production and Canadian labour data ahead. But given an event risk heavy week ahead, today’s run which also has a few ECB speakers may end up being just so much water under the bridge, though agricultural commodity markets will be very much focussed on the monthly USDA WASDE report, which follows on from China’s Agriculture Ministry CASDE overnight. Next week brings the Fed, ECB and BoJ policy meetings, which accompany a very busy data run from US (CPI, Retail Sales, PPI, Industrial Production, NY & Philly Fed Manufacturing and Michigan Sentiment surveys), China (Retail Sales, FAI, Industrial Production & Property sector indicators), and UK (labour data, monthly GDP & activity data). Elsewhere there are final CPI readings in the Eurozone, along with German ZEW survey, Australia has labour data, and Japan looks to Trade and Machinery Orders. It remains the case that ‘market signals’ are very dissonant, with the S&P 500 yesterday entering a bull market, while interest rate markets, buffeted by the RBA and BoC rate hikes this week, and continuing to price in a Fed rate hike in July, but looking for a rate cut in Q4. It attests both to the overhang of excess central bank liquidity, at the same time as market liquidity conditions continue to deteriorate, and likely signals that the current period of low volatility, above all in equities, may prove to be the calm before the storm.

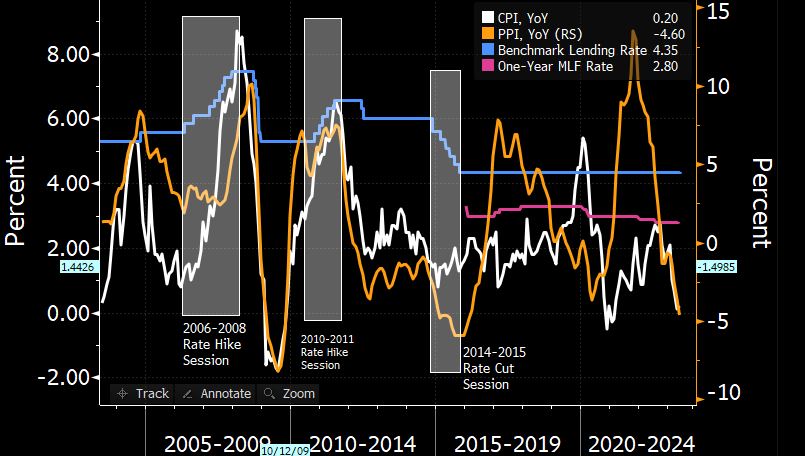

** China – May CPI & PPI **

The extent of the deflationary forces at work in China was above all evident in the m/m reading for PPI at -0.9% m/m and CPI at -0.2% m/m, which translate to y/y readings of PPI -4.6% y/y and CPI at 0.2%, the latter only edging up from 0.1% thanks to Food CPI base effects (1.0% y/y vs. April 0.2%), though Food PPI decelerated sharply to 0.2% y/y from 1.0%. The data has unsurprisingly fuelled expectations of a rate cut at next week’s 1-yr MTLF operation and the week after’s monthly Loan Prime Rate fixings, with major banks having already cut deposit rates. But as the example of the Eurozone during the previous decade amply demonstrates, all too often this leads to consumers doubling down on saving, rather than encouraging spending. Without major fiscal stimulus, which China’s authorities are clearly reticent to implement due to already dangerously high municipal debt levels, as well as fear of fuelling a speculative wave in its financial markets, a 5-10 bps cut in rates is likely to achieve little, above all in the absence of measures to a) cut Youth Unemployment that stands above 20%, and b) a more forceful approach to balance sheet reconciliation in the still very beleaguered property sector.