Written Commentary

The Week Ahead – Preview:

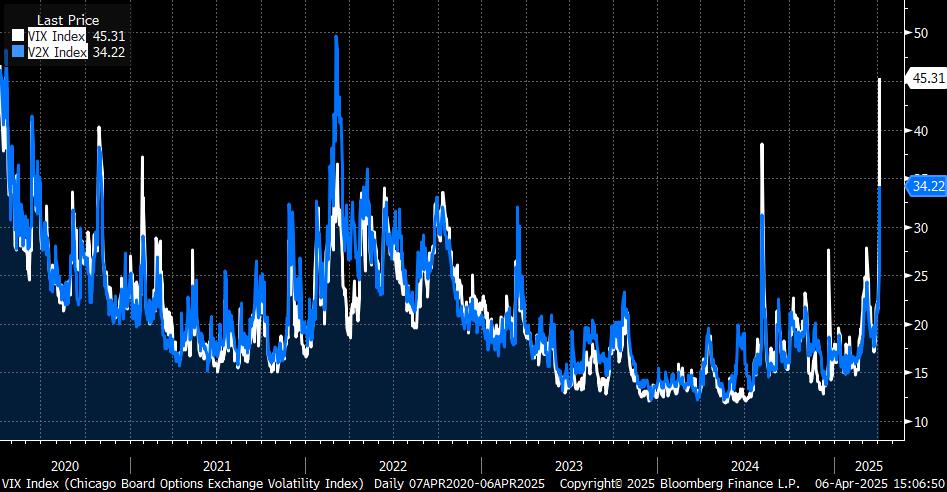

While the new week’s schedule has a good number of first division indicators in US, UK and China, as well as the start of the US Q1 earnings season, tariff wars will be front and centre, both in terms of retaliatory measures from other countries/regions, as well as the emerging dissent and popular unrest in the U.S., and how much further meltdown there will be in financial and commodity markets (see various charts attached). The run of statistics includes: US and China CPI and PPI, UK monthly GDP and accompanying activity indicators, German Industrial Production and Trade, China credit aggregates, Japan’s Labour Cash Earnings, PPI and Economy Watchers (services) survey, Indian Industrial Production and the Bank of Canada’s Q1 Business Outlook survey. As markets wait on the counter measures to US tariffs, the EU Trade Ministers Meeting on April 7 will be a focal point, and perhaps offer some signals on whether the EU is willing to escalate tensions with Digital and other Services taxes, or whether long standing internal tensions end up watering down its response, though in the first instance, it will try and negotiate with the US, though by all accounts the US administration has turned a deaf ear. FOMC minutes, the Bundesbank’s monthly report, an expected further 25 bps rated cut from India’s RBI, and plenty of central bank speakers tops the run of events. In the commodity space, US EIA’s monthly Short-term Energy Outlook (STEO) and the USDA’s WASDE and Brazil’s CONAB agricultural S&D reports will be closely watched; the IEA publishes its Energy and AI report, and there is a very busy run of energy, metals and agricultural energy conferences around the world (see commodities section in the calendar below).

– U.S.A.: One element of the rationale for US reciprocal tariffs that requires challenging is the unmitigated drivel about manufacturing. Let’s start with the conflation of lost manufacturing jobs with trade, to be sure outsourcing to China has a lot to answer for, but so does automation and digitalization, and proportionately major manufacturing countries such as Germany, Italy, Japan and South Korea have lost as many manufacturing jobs as the U.S. Then the claim that tariffs will create a lot of manufacturing jobs. Consider the following important points and make up your own mind: a) the IRA and CHIPS acts resulted in a ca. 140% increase in Manufacturing Construction Spending between Q3 2022 and end 2024, after flatlining since 2012 (see chart), admittedly with a lot of costly govt incentives, which the new administration wants to get rid of – but that increased capacity is already in place. b) That is a good thing, for those companies that have invested in increased capacity, and can utilize it to onshore production, but their supply chains will take considerable time to adjust. c) How large the shock to the US and global economies from tariff wars will be is written in the stars, but it will be substantial, though difficult to properly gauge until sometime in H2 2025, so rushing headlong into investing in additional capacity without an estimate of what the ROI and ROE will be is not going to happen. d) there is already considerable resistance to the tariffs from businesses and consumers, and they along with the political fraternity will already be weighing up whether these measures will survive until the mid-term elections in November 2026, be that as a result of judicial challenges or a volte face from those politicians facing re-election campaigns, and likely facing an angry reaction from the voting public. Now ask yourself, on a purely commercial basis, would you be rushing into investing in new capacity, or primarily looking at how you can re-purpose existing capacity? (By the way outside of Fed rate cuts in the face of an economic downturn, whenever the rollback comes, markets will roar, and supply chains be even more heavily disrupted by a sharp pick-up / rebound in demand, that will surely be inflationary, as per the example of the pandemic).

Be that as it may, this week’s US CPI and PPI will be combed for signs of tariffs impact, though ahead of these, one of the most partisan (pro-Republican) business surveys is published, NFIB Small Business Optimism, with the already published employment intentions falling to an 11-month low of 12 (down 3 pts) and all eyes on the Business Outlook which soared to a peak of 52 in December from -12 in September, though dipped back to 37 in February. Headline CPI is seen up 0.1% m/m, with energy (gasoline) a restraint and enabling a 0.2 ppt dip to 2.6% y/y, but core is expected to pick back up to 0.3% m/m, leaving the y/y rate unchanged at 3.1%, with core goods prices likely to be a key contributor, despite some easing in used car prices (unlikely to last given auto tariffs). PPI may prove to be the more obvious place to look for emergent price pressures, with headline forecast to edge back up to 0.2% m/m (vs. Feb Flat), and the y/y rate up 0.1 ppt to 3.2%, while core PPI is seen up 0.3% m/m to push the y/y rate up 0.2 ppt to 3.6%. The risks on core readings for both look to be to the upside, and by extension steeling the Fed’s determination to ‘wait and see’, though it will be increasingly sensitive to any signs that the sharp risk-off moves in financial markets may trigger a crisis type situation.

– U.K. / Eurozone – This week’s UK monthly GDP data are expected to exactly reverse January’s -0.1% m/m, which would see the q/q pace accelerate to 0.4% (from 0.2%), with Services, Industrial Production and Construction Output also all seen at 0.1% m/m – none of which are likely to make any impression on either the BoE or market expectations for UK rates. As previously noted there has been a steady improvement in Total Trade Balance, which needs to be monitored. After rebounding 2.0% m/m in January, German Industrial Production is expected to drop 1.0% m/m, with the dire profile of Factory Orders suggesting some downside risks, and Trade data are forecast to see a 1.5% m/m rebound in Exports after sliding 2.5% m/m in January, with Imports seen modestly lower m/m. As noted above, the primary point of focus will be the EU trade ministers meeting as potentially outlining the degree to which trade tensions with the US are likely to escalate.

– China / Asia: China’s CPI is expected to rebound to a still paltry 0.1% y/y, after sliding -0.7% y/y in February, with the sharp fluctuation owing everything to base effects due to the timing of the Lunar New Year holidays, but fundamentally underlining that weak consumer demand continues to ensure a lack of any price pressures. PPI is expected to edge down 0.1 ppt to -2.3% y/y, the 30th consecutive fall, with the stimulus measures that were announced at the National People’s Congress unlikely to feed through into either inflation measures until the latter half of Q2 2025.

– The Bank of Canada’s Q1 Business Outlook and Consumer surveys will be the other key highlight of the week, and offer some insights into how much impact the trade and other tensions with the US are impacting sentiment.

– There are 10 S&P 500 companies reporting this week, with worldwide corporate earnings highlights as compiled by Bloomberg News likely to include: Bank of New York Mellon, Blackrock, Cambricon Technologies, Constellation Brands, Delta Air Lines, Fast Retailing, Fastenal, JPMorgan Chase, Morgan Stanley, Qatar National Bank QPSC, Samsung Electronics, Seven & i, Tata Consultancy Services, Tesco, Wells Fargo, Zijin Mining Group.