Written Commentary

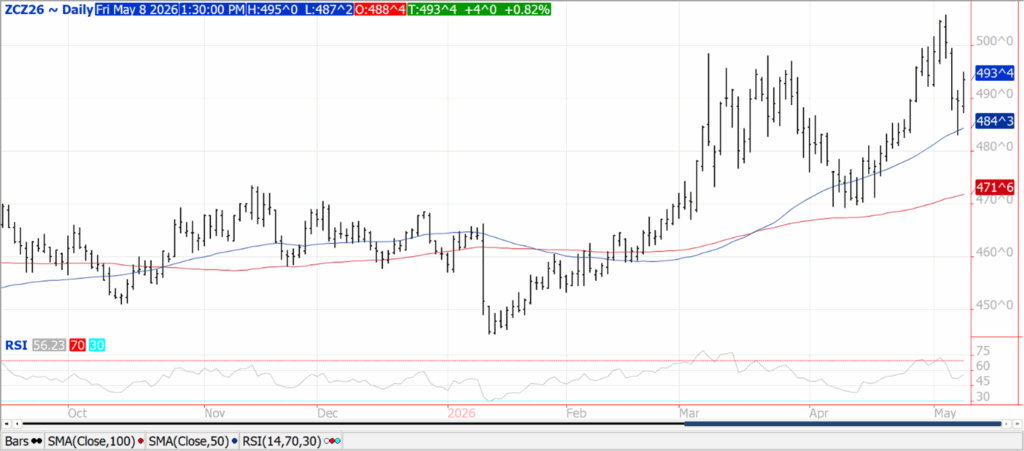

CORN

Prices were $.03-$.04 higher while spreads were mixed. Both July-26 and Dec-26 this week rejected trade below their respective 50-day MA’s. The trade expects little change in old crop ending stocks in Tues. USDA WASDE report. We look for a 25 mil. bu. cut to 2.102 bil. I see exports and feed usage up 25 mil. each with demand for ethanol down 25 mil. 2026 production is expected to fall nearly 1.1 bil. bu. to 15.935 bil. due to lower acres. I do not expect the trendline yield of 183 bpa from the Feb-26 Outlook Forum to change this month. The BAGE kept their Argentine production forecast unchanged at 61 mmt vs. the USDA est. of 52 mmt. Harvest progress has reached 30%. Look for higher global stocks in the USDA report on higher SA production. The US 26/27 export forecast from the Feb-26 Outlook Forum at 3.10 bil. bu. could be in jeopardy of being lowered if SA production is increased significantly.

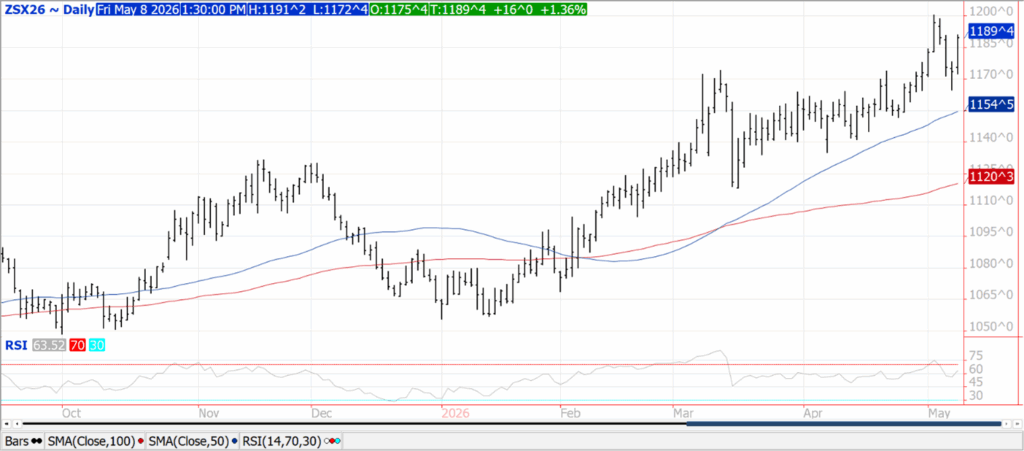

SOYBEANS

Prices were higher across the complex with beans up $.15-$.18, meal was up $1-$2 while oil was 15-25 points higher. Despite the strength, spreads eased across the complex. July beans also rejected trade below its 50-day MA this week while surging back above the $12 level. July-26 meal can’t seem to get too far away from its 50-day MA. Inside trade for July oil. Fueling today’s higher trade was a rebound in energy prices along with speculative buying ahead of next week’s USDA WASDE and production data, and Pres. Trump’s visit to Beijing late in the week. In addition today’s jobs report calmed fears that higher energy prices may lead the global economy into recession. Crush margins calculated off the July contracts at $3.13 bu. were down another $.12 today. Bean oil PV held at 53.8%. I expect the CFTC will print another record large, long position by MM’s in soybean oil and across the soybean complex. While the trade will continue to monitor developments in the ME, attention is shifting to Pres. Trump’s meeting with Chinese leader Xi late next week in Beijing. Without additional old crop sale to China, the USDA soybean export forecast at 1.540 bil. bu. is likely too large. I remain optimistic China will honor their commitment to buy at least 25 mmt of US soybeans over the next 3 MY’s. I look for a 20 mil. bu. shift from exports to crush, keeping US stocks near 350 mil. bu. The Ave. guess in the Reuters poll shows old crop ending stocks slipping 5 mil. bu. to 345. New crop production is expected to increase just over 180 mil. bu. to 4.445 bil. with trendline yields holding at 53 bpa. The BAGE kept their Argentine production forecast unchanged at 48.6 mmt, vs. the USDA est. of 48 mmt. Harvest progress jumped 16% to 34%, still just below the historical average of 39%. Brazil’s Ag. Ministry reports their exports in April-26 at 16.75 mmt, a new all-time record, up from 16.1 mmt shipped in April-21.

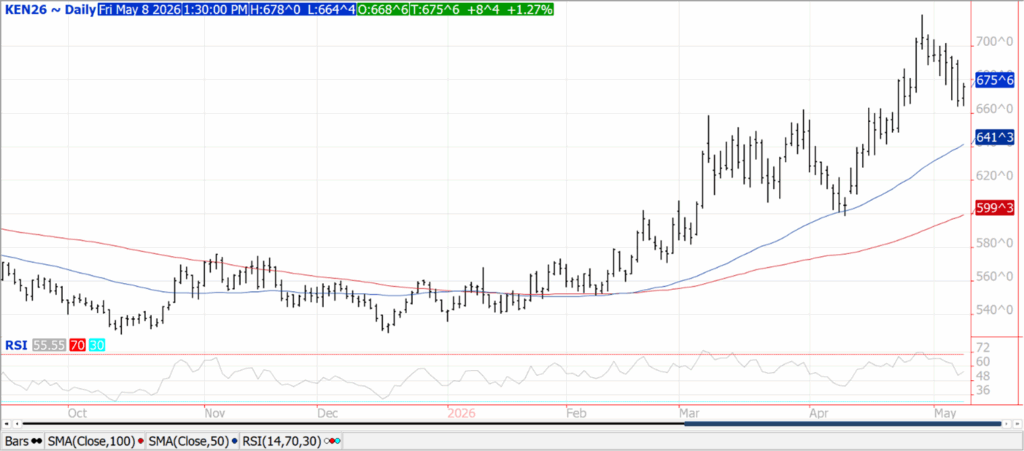

WHEAT

Prices ranged from $.05-$.09 higher with all 3 classes experiencing 2-sided trade. CGO July-26 is up $.06 ¾ at $6.19, KC July-26 was $.08 ½ higher at $6.75 ¾, while MIAX July-26 was up $.04 ¾ at $6.78 ½. I see no changes in old crop stocks, holding at 938 mil. bu. My all-wheat production forecast at 1.730 bil. is down 130 mil. from the Feb-26 Outlook and down 255 mil. from YA. My winter wheat production forecast at 1.185 bil. bu. is down 217 mil. from YA. By class production: HRW – 605 mil., SRW – 345 mil. and white – 235 mil. I look for US 26/27 ending stocks to fall to 850 mil. bu. My forecasts are all reasonably close to the Ave. est. in the Reuters poll. Ratings in Kansas have been in a steady fall all spring. IKAR cut Russia’s 25/26 export forecast 1.5 mmt to 44.5 mmt, falling in line with the USDA est. The UN Food and Agriculture Organization forecasts global production will fall 2% in 2026 to 817 mmt.

Risk Warning: Investments in Equities, Contracts for Difference (CFDs) in any instrument, Futures, Options, Derivatives and Foreign Exchange can fluctuate in value. Investors should therefore be aware that they may not realise the initial amount invested and may incur additional liabilities. These investments may be subject to above average financial risk of loss. Investors should consider their financial circumstances, investment experience and if it is appropriate to invest. If necessary, seek independent financial advice.

ADM Investor Services International Limited, registered in England No. 2547805, is authorised and regulated by the Financial Conduct Authority [FRN 148474] and is a member of the London Stock Exchange. Registered office: 3rd Floor, The Minster Building, 21 Mincing Lane, London EC3R 7AG.

A subsidiary of Archer Daniels Midland Company.

© 2021 ADM Investor Services International Limited.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.