Written Commentary

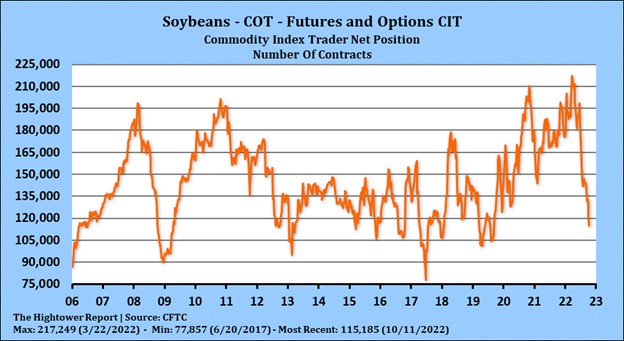

SOYBEANS

Soybean and soymeal futures are lower. Today is a risk off day with concern that recession will slow US soybean export demand. US harvest is near 63 pct and ahead of normal. The crushers have the best bid. Drop in US Miss river levels have forced soybeans back into the country. Talk of higher crush has collapsed US domestic soymeal basis. Talk of higher US biofuel use is helping soyoil prices. Some feel soybean futures rally may be limited unless there is a South America weather problem. Informa est US 2023 soybean acres at 88.5 vs 87.4 in 2022. They are using a US 2023/24 soybean carryout near 394 mil bu vs 246 this year.

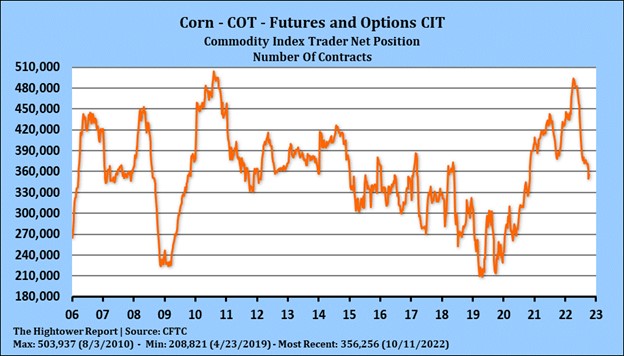

CORN

Corn futures ended lower. CZ dropped below 20 DMA near 6.82. Slow US export demand offers resistance. Low river navigation has forced corn back into the country. In some locations, corn basis has dropped from +100 to -100. Farmers are not selling and there is a good carry in cash corn prices to encourage farmers to store corn. US corn harvest is 45 pct which is behind normal. US Midwest weather should be dry and open for harvest. Argentina corn plantings are behind normal but rains are in the forecast. Fact Biden administration is expected to release US oil reserves is weighing on corn futures. Informa est US 2023 corn acres at 91.9 vs 88.6 in 2022. They have been using a 2023/24 US corn carryout near 1,918 mil bu vs 1,213 this year. This is due to a crop near 15,156 mil bu vs 13,344 this year, feed and residual near 5,650, ethanol use near 5,300 and exports near 2,000. The demise of La Nina could suggest a normal 2023 US Weather/trend yield. Trend yield is near 181 vs 172 this year. Since their peak, Managed funds have sold 160,000 corn contracts.

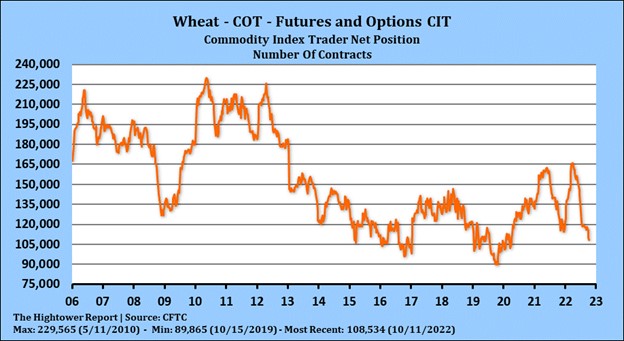

WHEAT

Wheat futures ended lower led by Chicago. Slow demand for US wheat exports and higher Russian supply offsets dry US and Argentina wheat areas. Trade still looking for new news on if Russia will extend Ukraine export corridor. Some feel latest is the corridor will remain open but no shipments to EU. US may impose sanctions on Turkey for importing stolen Crimean wheat. US wheat export forecast is lowest in 50 years. Informa est US 2023 wheat acres at 47.3 vs 45.7 in 2022. Informa is using a 2023/24 wheat carryout near 667 mil bu versus 576 this year. This includes a crop of 1,925 mil bu vs.1,650 last year. They do est an increase in exports to 815 vs 790 this year. This year’s exports are the lowest in 50 years.

See more market commentary here.

Risk Warning: Investments in Equities, Contracts for Difference (CFDs) in any instrument, Futures, Options, Derivatives and Foreign Exchange can fluctuate in value. Investors should therefore be aware that they may not realise the initial amount invested and may incur additional liabilities. These investments may be subject to above average financial risk of loss. Investors should consider their financial circumstances, investment experience and if it is appropriate to invest. If necessary, seek independent financial advice.

ADM Investor Services International Limited, registered in England No. 2547805, is authorised and regulated by the Financial Conduct Authority [FRN 148474] and is a member of the London Stock Exchange. Registered office: 3rd Floor, The Minster Building, 21 Mincing Lane, London EC3R 7AG.

A subsidiary of Archer Daniels Midland Company.

© 2021 ADM Investor Services International Limited.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.